Investors can often see them coming weeks in advance, but the specific amount of a given annual dividend hike is always a surprise. That’s because so much goes into management’s decision about this payout boost, beyond simply the most recent growth and earnings performance.

PepsiCo (PEP -0.34%) and Home Depot (HD 1.98%) each announced new dividend payment rates as part of their Q4 earnings updates in February. Let’s look at what these moves say about the business of these two companies and whether the dividend stocks are buys today.

1. PepsiCo

PepsiCo recently ended a solid year on a down note. Organic sales gains in the Q4 period slowed to a 5% year-over-year increase from 9% in the prior quarter, and investors are bracing for further sluggishness ahead. CEO Ramon Laguarta and his team say that sales will rise by just 4% in 2024 compared to last year’s 10% spike.

Demand trends in the beverage and snack food niches are slowing back down to the pre-pandemic pace after several years of above-average growth, but Pepsi’s dividend is still well covered by its ample earnings and cash flow. The company generated $13 billion of operating cash last year, up from $11 billion in 2022. That success was powered by improving efficiency and rising prices. “We are pleased with our results for 2023,” Laguarta said in early February.

Pepsi’s 7% dividend boost is covered by the expected 8% earnings increase in 2024. It’s true that the hike marked a slowdown compared to last year’s 10% dividend boost. Yet income investors should still be happy with the rising payout. Pepsi is among the most consistent dividend stocks on the market when it comes to annual raises. The 2024 boost was its 52nd consecutive annual hike.

2. Home Depot

A lot has changed since late February of 2023, when Home Depot announced its 10% dividend hike. Consumer spending slowed in the home improvement market as interest rates jumped and the housing market contracted. That pressure shows up most directly in Home Depot’s comparable-store sales, which fell 3% on the year.

The good news is customer traffic trends improved to a 3% drop from a 5% decline in 2022. However, average spending rates were down this past year as do-it-yourself shoppers canceled or delayed their home investment projects. It didn’t help that lumber prices collapsed year over year, either.

Yet Home Depot’s management team is still optimistic about the next several years. Operating profit margin is projected to hold above 14% of sales in 2024, putting the metric near the pandemic record of about 15% of sales. But with earnings on pace to decline for a second straight year, how could Home Depot afford to boost its dividend by 8% in 2024?

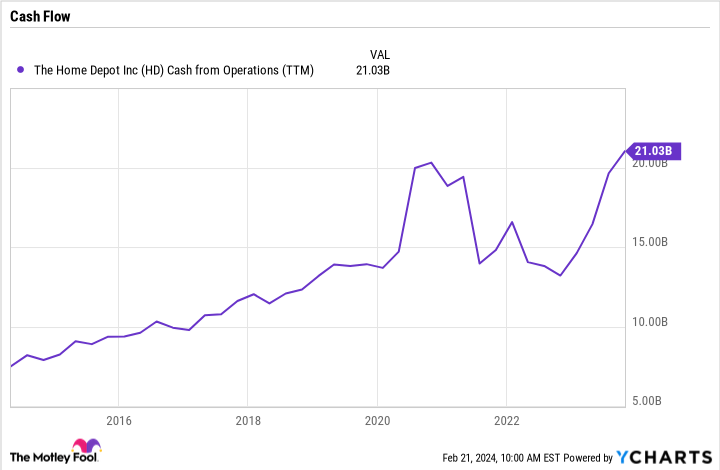

The short answer is cash flow. Home Depot became much more efficient last year as management adjusted to slowing sales trends. That explains how operating cash flow jumped to $21 billion from $15 billion on the year. This success allowed it to spend more on its dividend and stock buybacks without harming its financial position.

HD Cash from Operations (TTM) data by YCharts

Home Depot has a more diversified business than rival Lowe’s, which doesn’t generate as much revenue from the professional contractor niche. That difference, combined with its market-leading industry position, should allow the chain to keep winning share even in a tough selling environment. Investors can consequently expect many more years of dividend increases ahead, powered by that diverse business.

Demitri Kalogeropoulos has positions in Home Depot. The Motley Fool has positions in and recommends Home Depot. The Motley Fool recommends Lowe’s Companies. The Motley Fool has a disclosure policy.

{kind=link}