- Markets continue their downward momentum despite a positive start to the Q1 earnings season

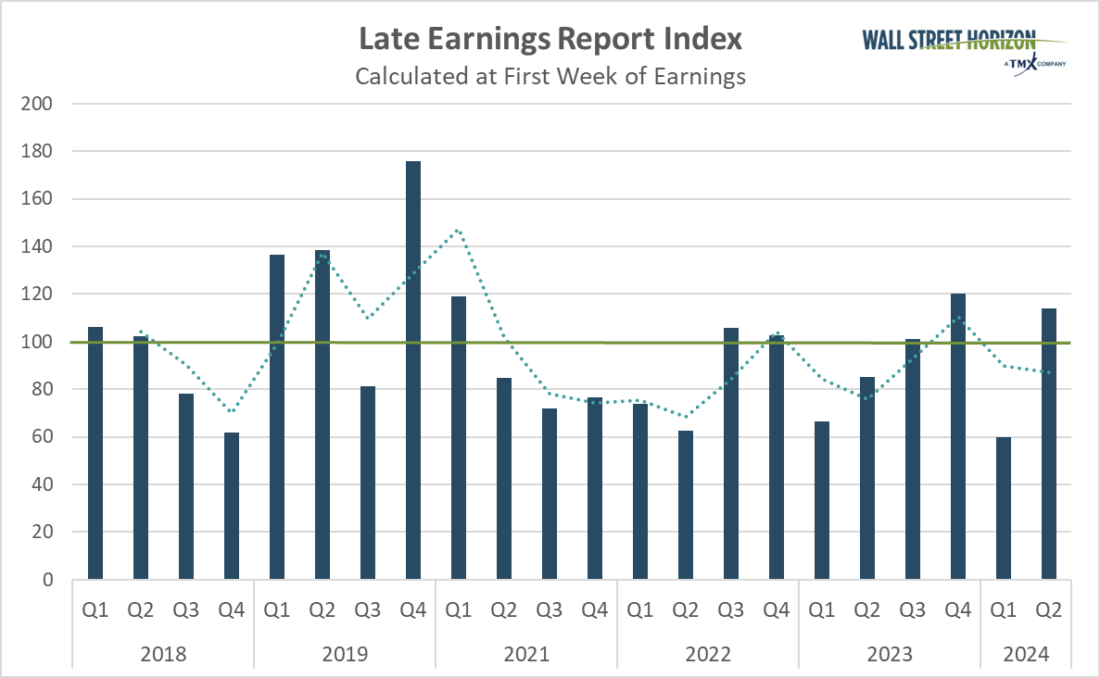

- The LERI shows corporate uncertainty ticking back up after falling in Q4

- All eyes turn to the Magnificent 7: Tesla (TSLA), Meta (META), Alphabet (GOOGL) and Microsoft (MSFT) out this week.

- Peak weeks for Q1 season run from April 22 – May 10

US markets continued their downward trajectory last week, even in the face of some decent earnings reports. The S&P 500® headed for its longest losing streak of the year, down for six consecutive days, as investors continued to focus on inflation, Fed commentary and the sinking realization that interest rate cuts might not come until 2025.

Stand-out earnings last week came from the investment banks, Goldman Sachs (GS) and Morgan Stanley (MS) on Monday and Tuesday, and continued with better-than-expected results from United Airlines (UAL) on Tuesday afternoon. The international carrier’s stock jumped 17% after they forecasted Q2 expectations well ahead of Wall Street estimates, signaling a strong start to peak travel season.1

The party continued on Thursday with robust results from tech and communication services names. Taiwan Semiconductor Manufacturing (TSMC) reported robust results on the top and bottom-line before-the-bell on the back of strong AI chip demand.2 Another highly anticipated name, Netflix (NFLX), was out after the bell. Impressive results showed their crackdown on password sharing continued to pay off when total subscribers jumped 16% in Q1.3 Even so, the stock sank following the report, as Netflix said they would no longer report that paid memberships metric starting in 2025 and investors continued to focus on inflation and geopolitical tensions.

Despite better-than-expected results last week, downward revisions to companies that have yet to report lead to a decrease in the blended S&P 500 EPS growth rate for Q1. According to FactSet, the current consensus is for 0.5%, an increase from 0.9% last week. Thus far 74% of companies that have reported have surpassed analyst estimates.4

Despite better-than-expected results so far this quarter, investors are rewarding companies with positive surprises by less than average, and punishing negative surprises by more than average. So what gives? Well it’s all likely in the commentary. While many companies have been able to put up impressive results for profits and sales, forward-looking guidance and overall commentary have been much more cautionary.

Our proprietary Late Earnings Report Index (LERI), has picked up on that trend and is highlighting how US CEOs may be more uncertain in Q2 as compared to last quarter.

The LERI tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, anything above that indicates companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests companies feel they have a pretty good crystal ball for the near-term.

The official pre-peak season LERI reading for Q1 (data collected in Q2) stands at 114, back above the baseline reading, suggesting companies are feeling less certain about economic conditions than they were at the beginning of the year. As of April 12, there were 43 late outliers and 34 early outliers.

It will be all about big tech this week, more specifically the Magnificent 7, of which four constituents are reporting. On the docket we have: Tesla (TSLA) out with Q1 2024 results on Tuesday after the bell, followed by Meta (META) out AMC on Wednesday and Microsoft (MSFT) and Alphabet (GOOGL) closing out the week on Thursday after the close. Intel (INTC) is not in the Magnificent 7, but it is expected to post one of the highest growth rates in the S&P 500 tech sector due to continued demand for generative AI products. According to FactSet, the tech behemoth is anticipated to show EPS growth of 475% YoY.

This season peak weeks will fall between April 22 – May 10, with each week expected to see over 1,500 reports. Currently May 9 is predicted to be the most active day with 1,236 companies anticipated to report. Thus far 59% of companies have confirmed their earnings date (out of our universe of 10,000+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

—

Originally Posted April 22, 2024 – The Magnificent 7 Get Set to Report Amidst an S&P 500 Losing Streak

1 United Airlines Announces First-Quarter 2024 Financial Results; Exceeds Revenue and EPS Expectations, April 16, 2024, https://www.united.com

2 TSMC Reports First Quarter EPS of NT$8.70, April 18, 2024, https://investor.tsmc.com

3 Netflix Q1 2024 Shareholder Letter, April 18, 2024, https://s22.q4cdn.com

4 Earnings Insight, FactSet, John Butters, April 19, 2024, https://advantage.factset.com

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}