Rate watchers are penciling in a 25-bp reduction by the Fed seven days from today on the back of this mornings mixed inflation data, as annualized price pressures arrived at the lowest level in over three years even with shelter costs accelerating meaningfully. Against this backdrop, equity players are pressing sell following the CPI release, because they are worried that the Fed may be too late in providing relief. Still, however, stock bulls should favor a slow and controlled vertical walk down the monetary policy stairs rather than a speedy and turbulent roll south to lower stories. Indeed, when performing historical analysis, the former case has been consistent with soft landings and earnings buoyancy, while the latter tends to occur during economic slowdowns and profit declines.

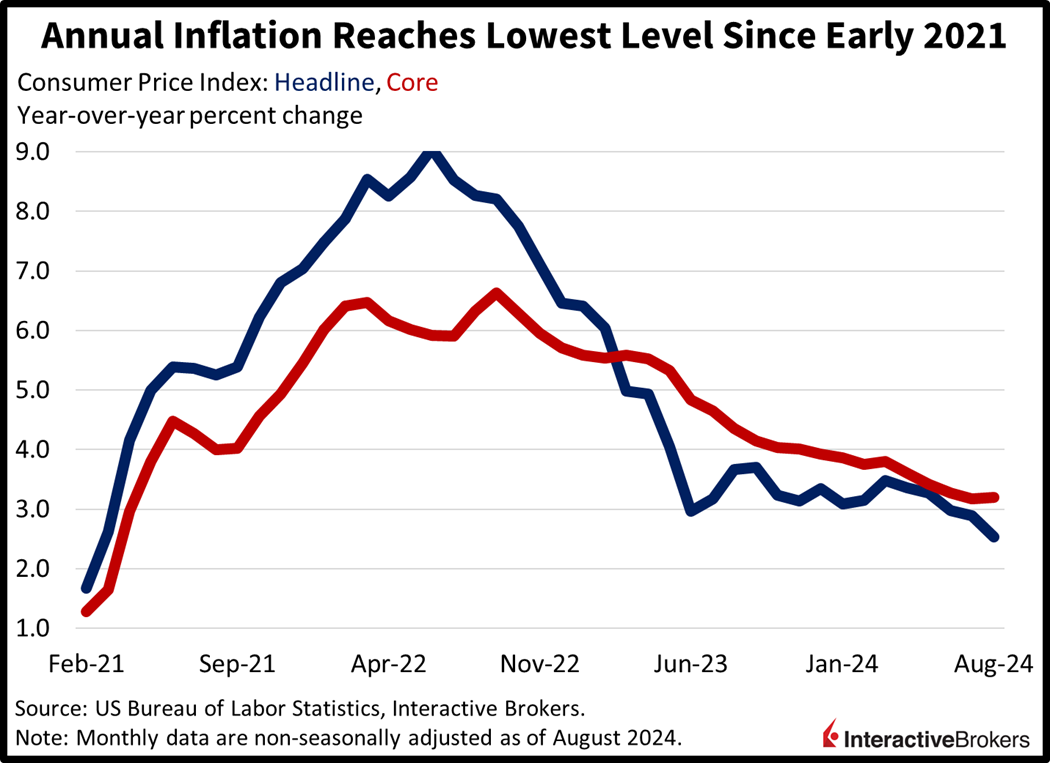

CPI Carries a Firm 2-Handle

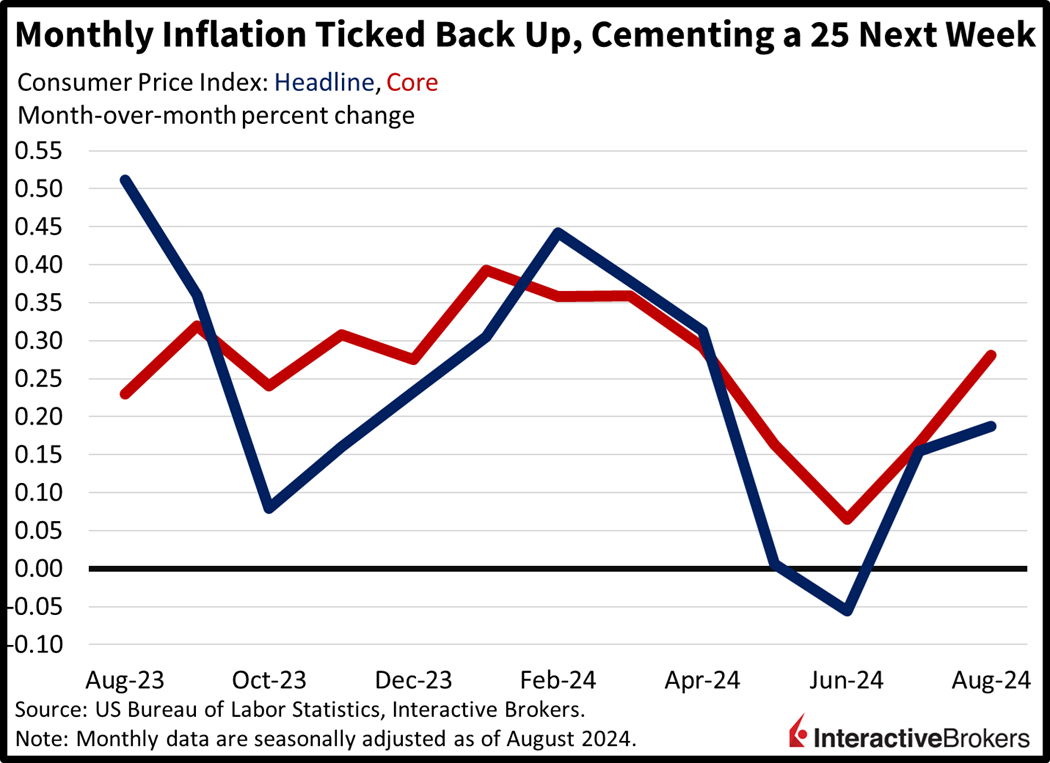

This morning’s Consumer Price Index (CPI) offered welcome progress, reflecting the lowest rate of yearly inflation since March of 2021. Prices rose 0.2% month over month (m/m) and 2.5% year over year (y/y) in August, in-line with projections on the former and 10 basis points (bps) lighter on the latter. Core stickers, which exclude food and energy due to their volatile characteristics, increased 0.3% m/m and 3.2% y/y, 10 bps heavier on the monthly figure and exactly as anticipated for the yearly result. In comparison, July’s result came in at 0.2% m/m and 2.9% y/y for headline and 0.2% m/m and 3.2% y/y for core.

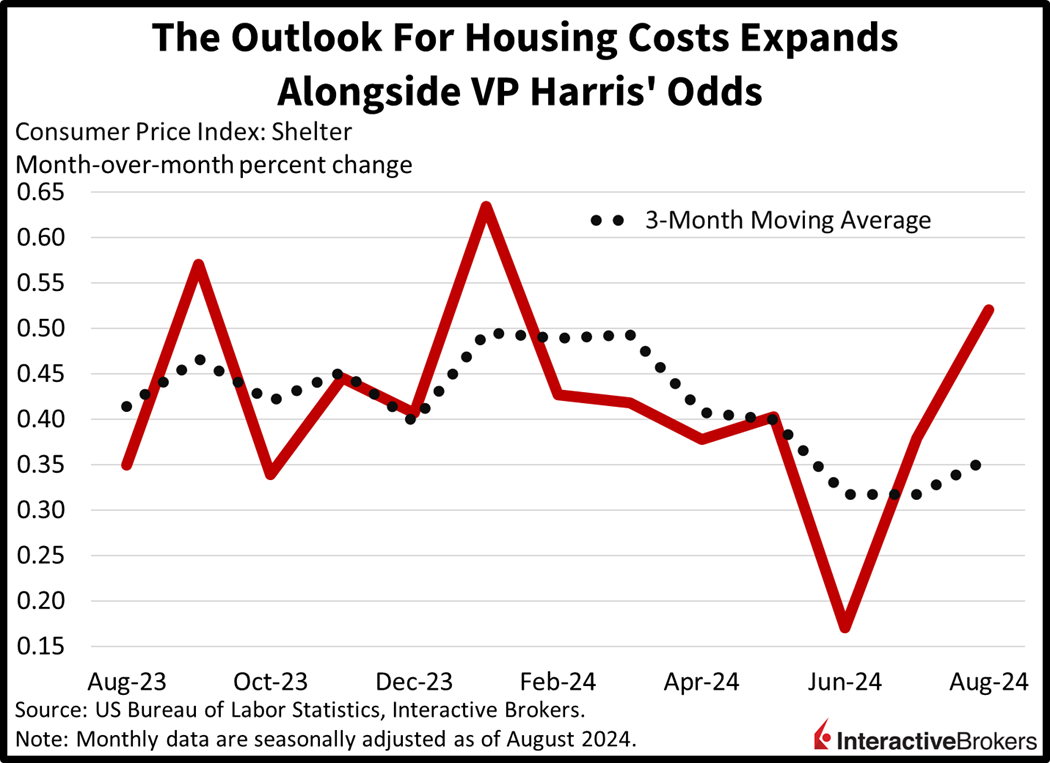

Transportation and Shelter Lead Price Pressures

Looking under the hood, outcomes were mixed across categories. Driving costs to the upside were transportation services, shelter, food at dining establishments and apparel, which saw charges climb 0.9%, 0.5%, 0.3% and 0.3%. Meanwhile, used automobiles, energy services (heating & electricity), gasoline and medical care services experienced m/m declines of 1%, 0.9%, 0.6% and 0.1%. New cars and food at the market were unchanged during the period.

Stocks Selloff but Lumber Jumps

Markets are reacting negatively to the data with stocks sinking while yields and the dollar rise. All major US equity indices are dropping and the rate-sensitive areas are suffering the most. The Dow Jones Industrial, Russell 2000, S&P 500 and Nasdaq Composite are lower by 1.2%, 1%, 0.8% and 0.3%. Sectoral breadth is negative with every segment losing on the session being led by financials, energy and real estate which are all lower by 1.8%. Treasurys are being sold modestly, with the 2- and 10-year maturities changing hands at 3.62% and 3.64%, 2 bps heavier on the shorter-end and unchanged on the longer. The greenback is up 6 bps as it appreciates versus the euro, pound sterling, franc and Aussie and Canadian dollars but depreciates against the yen and yuan. What’s most concerning from a currency perspective is that the yen is now stronger than it was during the early August carry trade selloff. It reached 140.70 this morning against its US counterpart, much firmer than the 141.68 that it reached on August 5. Commodities are moving higher for the most part, with lumber, copper and crude oil up 4.4%, 0.5% and 0.3% but gold and silver are lower by 0.5% each. Lumber is up sharply on the back of Vice President Kamala Harris’ odds jumping sharply following last night’s debate as well as this morning’s unexpected jump in shelter costs. Homebuilders are positioning for the continuation of substantial immigration flows and further upside for home prices and rents by scooping up the vital construction material.

Shelter is a Huge Deal

Today’s inflation data is encouraging overall, but caution regarding price pressures, is warranted. This is particularly significant with shelter, which has shown persistent cost increases, a trend that is likely to continue. The US has suffered from a housing shortage for many years, a result of construction trailing the increasing numbers of individuals and families that are seeking homes. More recently, demand is being supported by substantial immigration flows and overall population growth while the resale market is extremely tight as homeowners with record-low mortgage rates are staying put rather than selling their dwellings and buying new residences with much more expensive financing. These trends are likely to support loftier prices, making the American Dream less attainable and causing many consumers to suffer from the fear of missing out. The elevated housing prices, moreover, are a significant threat to the Fed’s efforts to curtail inflation with shelter representing a significant portion of household budgets. Against the backdrop, rising odds of a Harris presidency, an immigration dove, further complicate the outlook for real estate affordability. Just look at the performance of lumber, a critical ingredient for construction.

To learn more about ForecastEx, view our Traders’ Academy video here

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}