A WSJ article has shifted market expectations … the importance of Fed forward guidance … the growing uncertainty about tomorrow … don’t miss the big picture

The drama surrounding the size of tomorrow’s interest rate cut has exploded over the last week.

What was a relatively sure thing just a handful days ago has been flipped on its head, and the potential for increased volatility tomorrow has spiked.

Let’s unpack this unfolding soap opera…

About one week ago, the market was betting big on just a quarter-point interest rate cut from the Federal Reserve at tomorrow’s September FOMC meeting

The matter was all-but settled. According to the CME Group’s FedWatch Tool, earlier this month, the probability of this single quarter-point cut stood at 85%.

So, why – only a short while later, following two inflation reports that, if anything, were hotter than expected – is the market now pricing in a 63% chance of a 50-basis-point cut?

Because of Nick Timiraos.

Now, you’re likely scratching your head right now. Who is Nick Timiraos?

Let’s rewind to a Digest from September of last year in which we featured analysis from our hypergrowth expert Luke Lango. He was referencing a Wall Street Journal (WSJ) article and its significance relating to upcoming Federal Reserve policy:

From Luke:

The WSJ article was important for one reason in particular. It was authored by Nick Timiraos – the so-called “Fed Whisperer”; nearly everything he writes about the Fed ends up being true…

And when I spoke with Luke in researching that Digest, he told me:

When Timiraos is hawkish, Powell’s hawkish. When Timiraos is dovish, Powell’s dovish. By design.

This brings us to last Thursday’s WSJ article from Timiraos, titled “The Fed’s Rate-Cut Dilemma: Start Big or Small?”

Did Timiraos intentionally let the cat out of the bag?

Let’s go to Timiraos’ WSJ article. And remember, going into this article, the question of the size of the interest rate cut was largely settled in the minds of Wall Street traders:

Federal Reserve Chair Jerome Powell faces a difficult decision as the central bank prepares to cut interest rates next week: Start small or begin big?

The central bank is set to reduce rates for the first time since 2020 at its meeting on Sept. 17-18. Because officials have signaled greater confidence that they can make multiple rate cuts over the next several months, they are confronting questions over whether to cut by a traditional 0.25 percentage point or by a larger 0.5 point…

Alternatively, officials could conclude that if they expect a 50-basis-point move is likely in November or December, they ought to make that move now, when rates are farthest from their ultimate destination…

[A fellow at the Center for Financial Economics at Johns Hopkins University] said he thinks the Fed could manage concerns about spooking investors with a larger cut by providing “a lot of language around it that makes it not scary.” He added, “It wouldn’t need to be a sign of worry.”

Now, though I highlighted some of the content that hinted at a 50-basis-point cut, Timiraos also gave lip-service to a 25-basis-point cut. But that’s the problem – he straddled the fence…with a slight edge going to 50.

Here’s how he ended his article:

“We are at a point where you might say, ‘I could go either way—25 or 50,’ but I think the risk management has shifted to the labor market and favors doing 50,” [Donald Kohn, a former Fed vice chair] said.

And just like that, Timiraos (or Powell?) threw the proverbial grenade into the mix.

Could the Fed have done a better job of signaling?

The Federal Reserve does not like to surprise the market. Therefore, it usually goes to great lengths to signal its upcoming policy moves.

It does this through “forward guidance,” which can be accomplished by official FOMC policy statements or through preferred members of the press, like Timiraos.

In any case, here’s former Federal Reserve Chairman Ben Bernanke from back in 2013, speaking to the link between Fed guidance and investor behavior, and its critical importance:

The public’s expectations about future monetary policy actions matter today because those expectations have important effects on current financial conditions, which in turn affect output, employment, and inflation over time.

For example, because investors can choose freely between holding a longer-term security or rolling over a sequence of short-term securities, longer-term interest rates today are closely linked to market participants’ expectations of how short-term rates will evolve…

In short, for monetary policy, expectations matter. Indeed, expectations matter so much that a central bank may be able to help make policy more effective by working to shape those expectations.

Guidance is intended to reduce exaggerated market volatility and confusion, not amplify it. But that’s not what just happened.

Various analysts have been scratching their heads and frowning about the impact of this “last minute” article. For example, here’s analyst Jim Bianco from a post on LinkedIn:

Timiraos is considered the fed’s mouthpiece. Instead of clarifying, which is what is what his stories are intended to do, it took us from 14% to 50%, the maximum point of uncertainty.

In other words, the fed’s mouthpiece in an era of forward guidance did the opposite of providing clarity…

From the Fed’s perspective, Friday’s fed fund futures close was about the worst possible: 49% probability of a 50 bps cut/51% probability of a 25 bps cut (chart). This is literally one tick from maximum uncertainty (50/50).

About half of Wall Street will be disappointed/surprised if this holds through Wednesday.

The Fed designed forward guidance (tell them what will happen before you do it) to prevent this exact scenario.

In the comments underneath Bianco’s post, the conversation grew lively. One reader wrote:

Since when is it the Fed’s mandate to please or not surprise Wall Street? Forward guidance is supposed to be dead…

Bianco shot back:

Forward guidance is not supposed to be dead. It’s supposed to be the guiding principle.

Now, if they want to end guidance, I don’t have a problem with it. But you don’t do it with a haphazard Nick Timiraos story on some Thursday morning a week before the meeting when no one expects it.

Due to the sudden confusion, Bianco suggested we would get a clarifying story this past Monday from Timiraos that would clear things up. Well, Bianco was wrong – the article came this morning…but it didn’t remove the uncertainty.

Once again, Timiraos tap-danced on both sides of the issue. But in my opinion, he wrote nothing to forcefully steer expectations back to just 25 basis points.

What I found most interesting was how much gray area Timiraos allowed to remain. Here are a few examples:

- Because the decision this week is a close call, Powell could face at least one dissent on the decision from the 12 policymakers—five reserve-bank presidents and seven Washington-based governors—who vote on policy…

- That this week’s decision is a close call could reflect honest uncertainty over the right choice…

- “You have a bunch of people who are genuinely uncertain what the right thing to do here is,” he said. “In the end, Powell can probably build a reasonable consensus around either.”

Timraos might be the Fed’s mouthpiece, but it’s a rather muffled mouthpiece this time.

Regardless of the debate about forward guidance, what’s clear is that stock prices jumped higher in the wake of last week’s Timiraos’ article

The Nasdaq added nearly 2% last Thursday and Friday as expectations for a 50-basis points cut spiked. And earlier today, it was up almost another 1% (though it’s pulling back as I write early-afternoon). So, whether Powell wanted it or not, many traders are now looking for (and positioned for) a 50-basis-point cut.

Of course, if Powell follows through, what will that signal about the health of our economy? Why are 50 basis points needed if everything is hunky dory and we’re about to enjoy a soft landing?

You’d expect Powell to provide an abundance of flowery hedging language in his press conference to talk down such questions.

But if Powell gives us just 25 basis points after winking and nodding at 50 through Timiraos, what was all this about? Roughly a week ago, this wasn’t an issue. Wall Street had accepted 25 basis points. So, why throw the grenade at all if there wasn’t to be any follow-through?

Here’s the latest meme on the sudden repositioning in the market based on this, comparing Powell to the oblivious, simple-minded Ralph Wiggum from The Simpsons…

So, how will this play out?

If I was in a friendly wager, I would bet on a 50 basis-point cut, followed by some selling. To be clear, I’m not sure how much of that selling would come from simple “sell the news” profit-taking versus legitimate surprise at the policy.

Bottom line: Given the tightknit relationship between Powell and Timiraos, the WSJ story wasn’t accidental, nor was this morning’s follow-up article that didn’t push expectations back to 25 basis points.

Powell knows that if he doesn’t follow through with 50, Wall Street traders will have good reason to be dismayed.

Regardless of the size of the cut tomorrow and whatever volatility it might bring, let’s remember the bigger picture

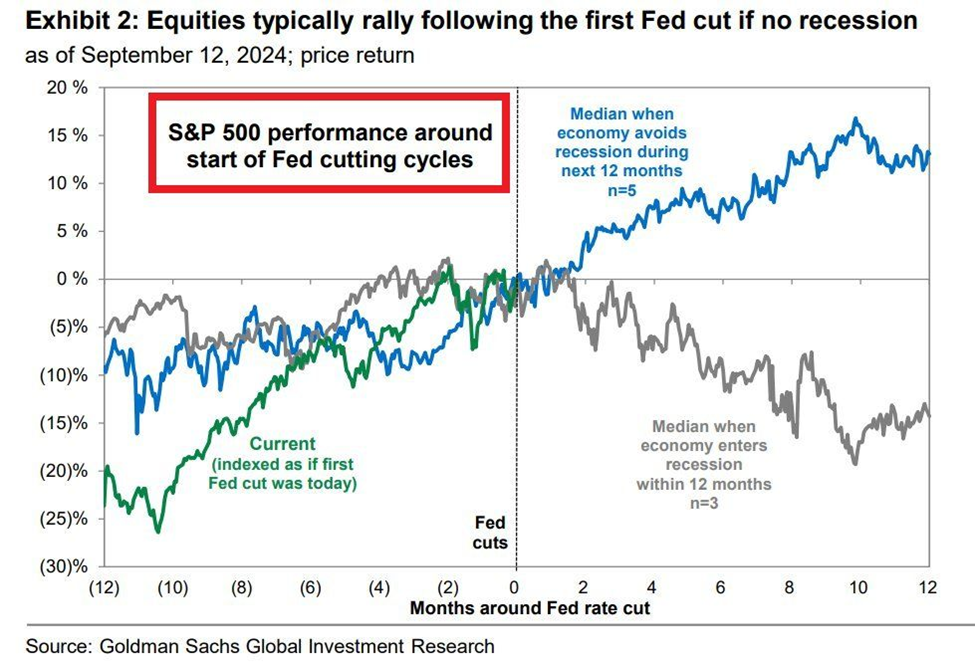

Rate cuts are good for stocks…if we can avoid a recession in the next 12 months.

The following chart shows the binary…

The median 12-month market return when we avoid a recession is about 10%. But if we do have a recession, the median 12-month return is a loss of about 15%.

Meanwhile, keep in mind, the entire world is on the verge of more cuts. In fact, get ready for the largest global rate-cutting cycle since covid.

Six out of 10 of the world’s top central banks have been cutting interest rates this year, and more cuts are coming.

History suggests this should be good for your portfolio in the longer-term.

As for the shorter-term, well, get your popcorn ready. We have a great drama unfolding thanks to Powell and Timiraos.

Have a good evening,

Jeff Remsburg

{kind=link}