Market participants are breathing a sigh of relief in response to this morning’s key inflation report. October’s CPI arrived exactly as anticipated, causing rate watchers to dial up the probability of another 25-bp Fed trim in December. Not so fast though, fixed-income performance is being heavily influenced by the duration profile of portfolios, with bifurcated action across the short and long ends. Indeed, a hastier projected walk down the Fed’s monetary policy stairs is coinciding with worries that tariffs and critical trade hawk appointees may reverse goods disinflation by disrupting existing commerce relationships. Still, sticky price pressure expectations aren’t interfering with the enthusiasm of the Trump trade, with cyclical stocks, value sectors and bitcoin outperforming today.

The Fed’s Inflation Battle Isn’t Done Yet

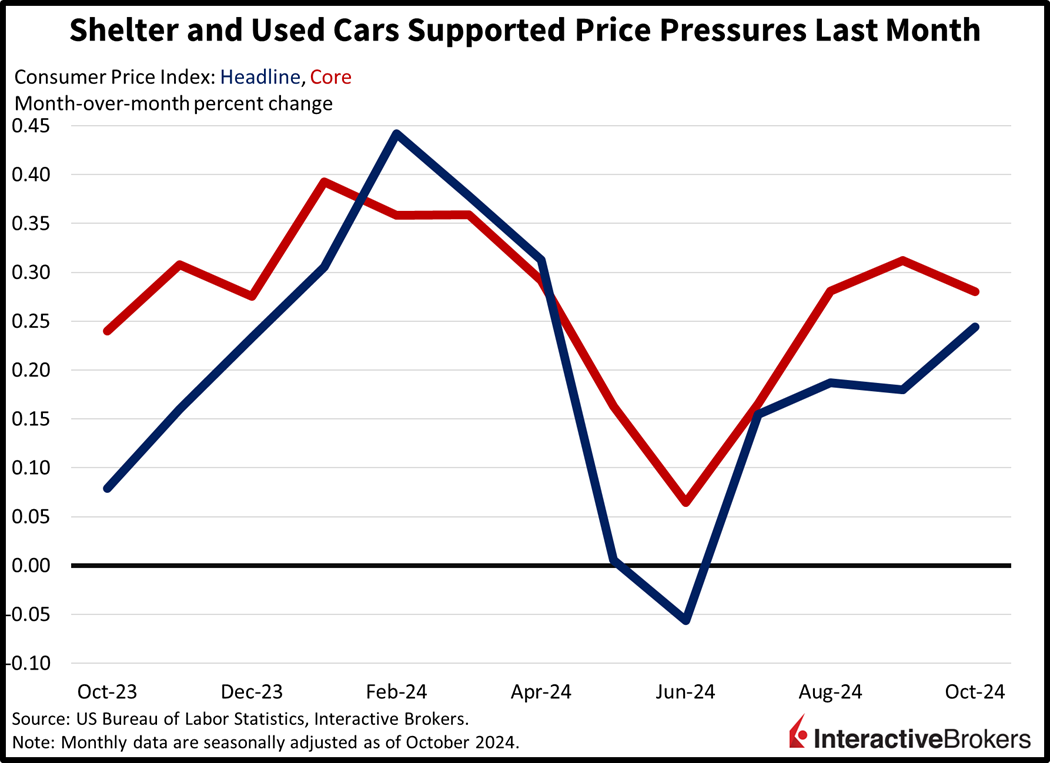

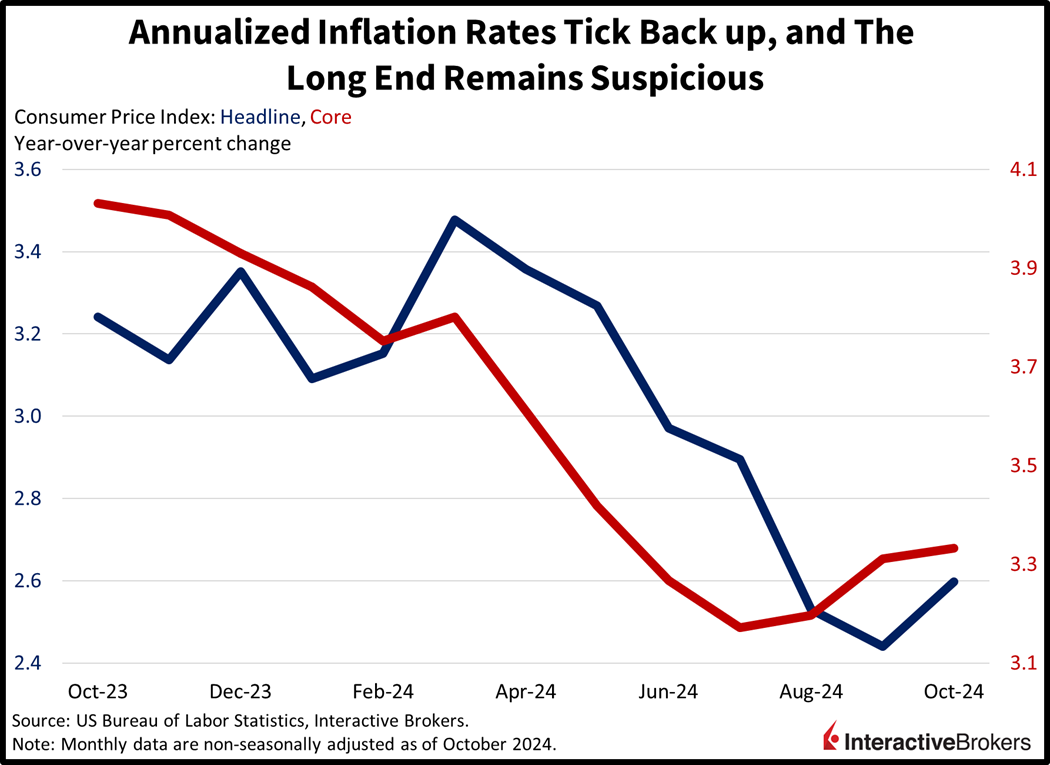

The Fed’s battle against inflation produced somewhat mixed results in October, with the Consumer Price Index (CPI) climbing 0.2% month over month (m/m) and 2.6% year over year (y/y). Both numbers matched expectations and the m/m result was unchanged from September; however, the 12-month figure increased from 2.4% in the preceding month. The core version of the indicator, which excludes food and energy due to their volatile characteristics, also matched estimates and was unchanged from September’s m/m and y/y gains of 0.3% and 3.3%, respectively. The used cars and trucks category climbed 2.7%, the largest increase among CPI constituents. Cox Automotive reports that the inventory at the start of October, at 2.15 million units, was down from 2.18 million m/m and fell 4% y/y. Hurricane Helene is suspected of increasing sales during the second half of September to replace flooded vehicles. Indeed, CARFAX (KMX) reports that as many as 138,000 were damaged during the storm.

Other categories with price gains and the amount of the increases were as follows:

- Energy services (electricity and heating), 1%

- Shelter, 0.4%

- Transportation services, 0.4%

- Medical care services, 0.4%

- Food at dining establishments, 0.2%

- Food at markets, 0.1%

Prices for new automobiles were unchanged while apparel and gasoline stickers contracted by 1.5% and 0.9%.

The Trump Trade Gains Steam

Despite lingering price pressures and trade uncertainty, markets are bullish during this strong seasonal period. The Trump equity baskets are leading this session with the cyclically tilted Russell 2000 and Dow Jones Industrial benchmarks gaining 0.6% and 0.3%. But the Nasdaq 100 and S&P 500 aren’t catching as much interest, with the former index down 0.3% while the latter is unchanged. Sector breadth is impressively positive with 9 out of 11 segments pointing north on the session and led by real estate, consumer discretionary and industrials; they’re up 1.2%, 0.8% and 0.6%. Technology and communication services are the laggards of the day; they’re lower by 0.2% and 0.1%. We’re witnessing bull-steepening action across the yield curve, with the 2- and 10-year Treasury maturities changing hands at 4.28% and 4.42%, 7 and 1 basis points (bps) lighter today. Softer interest costs aren’t weighing on the dollar, however, which is up a sharp 39 bps on the back of expected stateside economic outperformance. Indeed, Trump’s geopolitical and trade stances are expected to weigh on European activity, with the euro down to a one-year low versus the US currency. Meanwhile, the Dollar Index (DXY) this morning reached its tallest level since early May, as the American tender appreciates versus most of its major contemporaries, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian counterparts. Commodities are also mostly higher with lumber, crude oil, silver, and gold up 0.8%, 0.7%, 0.1% and 0.1%, while copper is bucking the trend; it’s down 0.8%. WTI crude is trading at $68.43, with its mild recovery being tempered by a weak demand outlook combined with expectations of abundant supplies.

Economists and Forecast Traders Diverge Over PPI

Looking ahead to the rest of the week, there’s plenty of Fed and ECB speak coming, including chief Powell, as well as critical domestic reports on wholesale prices, unemployment claims and retail sales. Tomorrow’s Producer Price Index (PPI) is certainly top of mind, with stock and bond bulls alike hoping that it reflects modest pricing pressures in the pipeline that can prop up rate cut expectations into 2025. Furthermore, one thing we noticed here at the economics desk is a wide discrepancy between the consensus PPI projection and the IBKR Forecast Trader threshold. Indeed, Wall Street is estimating a y/y figure of 2.3% while our Forecast Traders are much lower, with a PPI projection above 1.3% priced at just 75%. A figure of 1.3% would require a massive and highly unlikely 0.7% m/m decline in wholesale prices, or deflation, pointing to the potential for the Yes Forecast Contract to be correct and reward investors. Perhaps, our Forecast Traders believe that the October drop in gasoline and jet fuel costs will drive the headline much lower but getting to 1.3% is just a really narrow path for this specific report.

Source: ForecastEx

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ForecastEx

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx forecast contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

Disclosure: Forecast Contracts

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Hong Kong Limited, and Interactive Brokers Singapore Pte. Ltd.

Disclosure: ForecastEx Market Sentiment

Displayed outcome information is based on current market sentiment from ForecastEx LLC, an affiliate of IB LLC. Current market sentiment for contracts may be viewed at ForecastEx at https://forecasttrader.interactivebrokers.com/en/home.php. Note: Real-time market sentiment updates are only active during exchange open trading hours. Updates to current market sentiment for overnight activity will be reflected at the open on the next trading day. This information is not intended by IBKR as an opinion or likelihood of a potential outcome.

{kind=link}