In 2023, the megacap tech stocks known as the “Magnificent Seven” generated 58% of the cap-weighted S&P 500‘s 26% total return. In turn, many small- to mid-cap stocks lagged behind the overall market as inflation and higher interest rates created challenges for the companies with limited means and weaker balance sheets.

Considering the stock market’s cyclical nature, 2024 might be the year for small- to mid-cap stocks to turn their share prices around. So, with that in mind, let’s examine three stocks that struggled in 2023 and why I’m ready to buy them.

1. Crocs

The market is treating Crocs (CROX 0.73%) as if the manufacturer of casual shoes is just a fad, with its stock down about 22% over the past year. Despite the decline, the company is reaching new heights in sales and profitability, creating what appears to be an undervalued stock.

First, Crocs management recently released its updated 2023 sales projections, including expectations for $3.95 billion in revenue, an 11% jump from 2022. Crocs management also provided a sales outlook for 2024, including an estimate for 3% to 5% revenue growth from 2023.

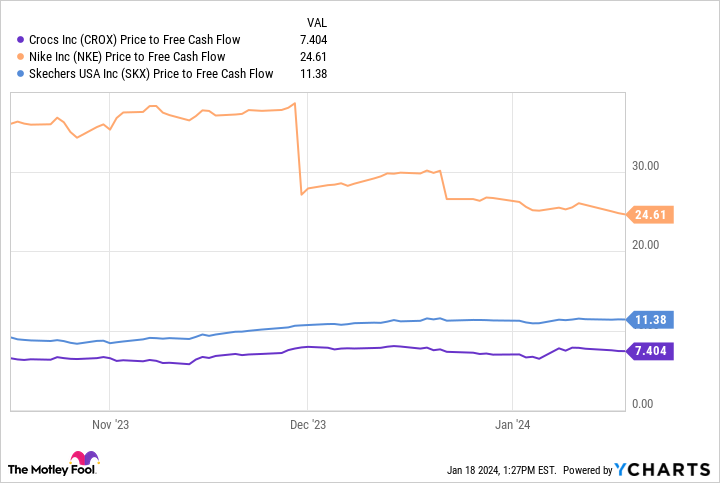

Another metric where Crocs is performing well is free cash flow, which demonstrates how much cash a company generates after supporting its operations and capital expenditures. For the trailing 12 months, Crocs generated $836 million in free cash flow, a high-water mark for the company. Using the valuation metric price-to-free-cash flow, Crocs looks cheaper than its competitors. Specifically, Crocs stock trades at only 7.4 times free cash flow, whereas shoe giant Nike trades at 24.6 times free cash flow and Skechers trades at 11.4.

CROX Price to Free Cash Flow data by YCharts

One concern for Crocs is its net debt (total debt minus cash and cash equivalents) in a high-interest rate environment. In early 2022, Crocs acquired competing casual footwear brand HeyDude for $2.05 billion in cash and about $500 million in stock. As a result, the company’s net debt skyrocketed from roughly $249 million to $2.7 billion. The good news is management is using its free cash flow to pay down its net debt, lowering it to about $1.5 billion at the end of 2023.

Skeptics may continue to question the staying power of Crocs, but with record-breaking results, a low valuation, and an improving balance sheet, its stock looks like a great buying opportunity at its current price.

2. Etsy

It’s been a tough couple of years for Etsy (ETSY 0.23%) shareholders. The stock for the online retailer specializing in unique goods is down about 46% during the past year and 76% from its all-time high in 2021.

Arguably, Etsy’s biggest misstep was its acquisition strategy between 2019 and 2021, buying three online platforms for about $2.1 billion. In the third quarter of 2022, Etsy took a $1 billion impairment charge for two of those acquisitions, musical instrument marketplace Depop and Brazil-based marketplace Elo7, meaning the company wrote off nearly half of its combined investment as a loss. Etsy completely divested Elo7 in 2023, selling it to a competing Brazilian online marketplace for an undisclosed amount. As a result of the acquisitions, Etsy’s balance sheet worsened from having $600 million in net cash at the end of 2020 to nearly $1.5 billion in net debt by its third quarter of 2021.

So why am I bullish on Etsy? The platform is adding to its active buyers and sellers again after facing a slump in 2022, leading to record revenue. But more importantly, Etsy continually generates strong free cash flow and trades at a rock-bottom valuation.

Etsy generated $2.71 billion in revenue over the trailing 12 months, representing a 6% increase from its 2022 annual revenue of $2.56 billion and a 14% increase from its 2021 annual revenue of $2.33 billion. Etsy’s $2.71 billion revenue translated to roughly $676 million in free cash flow, which the company has utilized to reduce its shares outstanding by nearly 5%, resulting in a higher ownership stake for shareholders.

Etsy management still needs to prove itself after its misstep with acquisitions. Still, the shares currently trades at 14.1 times free cash flow, close to an all-time low valuation, making the stock a potential rebound candidate.

ETSY Revenue (TTM) data by YCharts

3. Warby Parker

The last stock on this list is eyewear retailer Warby Parker (WRBY 0.46%), which is down 67% from its direct listing in late 2021 at $40 per share. The company has pivoted away from being an online-focused retailer into becoming a one-stop shop for all corrective vision needs after its growth stagnated in 2022.

The company opened 37 new stores during the past year, a 19% increase, bringing its total count to 227 locations. This strategy has resulted in a significant jump in revenue, which management projected to be between $666 million and $669 million for 2023, an increase of about 11.5% from 2022.

In addition to its growth, Warby Parker is positioned to navigate a high interest rate environment without resorting to debt. The company boasts a debt-free balance sheet, with a substantial $216 million in cash and cash equivalents as of its latest reported quarter. Moreover, the company is on track to report its first full year of positive free cash flow as a public company. Over the past 12 months, Warby Parker generated $16.9 million in positive free cash flow, representing a significant improvement from its 2022 negative free cash flow of $49.8 million.

One thing for investors to watch is Warby Parker’s share count. Since going public, the company has diluted its shares outstanding by 5.5% with its stock-based compensation packages. Considering management’s past history and limited free cash flow to repurchase shares, the trend is unlikely to reverse anytime soon.

Nevertheless, the strategic pivot undertaken by Warby Parker, leading to a resurgence in revenue growth alongside its robust balance sheet, positions its stock as a compelling candidate for a rebound.

Are these struggling stocks worth buying?

Investors should exercise caution when there’s a significant drop in any stock, recognizing there are usually legitimate concerns with the business or management when it occurs. Still, all three of these businesses have strong brands with loyal customers and, better yet, are reporting record revenue and free cash flows. So, as long as you take a long-term approach, these beaten-down stocks offer an opportunity for investors to buy into three strong businesses at fair prices.

Collin Brantmeyer has positions in Crocs, Etsy, Nike, and Warby Parker. The Motley Fool has positions in and recommends Etsy, Nike, and Skechers U.s.a. The Motley Fool recommends Crocs and recommends the following options: long January 2025 $47.50 calls on Nike. The Motley Fool has a disclosure policy.

{kind=link}