It’s been a great year for the broader indexes, but recent market volatility may have some investors wondering if now is a good time to sell stocks.

While it’s a mistake to let emotions dictate investment decisions, it’s always a good idea to ensure that the companies or exchange-traded funds (ETFs) you invest in have what it takes to navigate challenges or even endure a prolonged downturn. That way, you can rest easy knowing your investments are worth holding through periods of volatility.

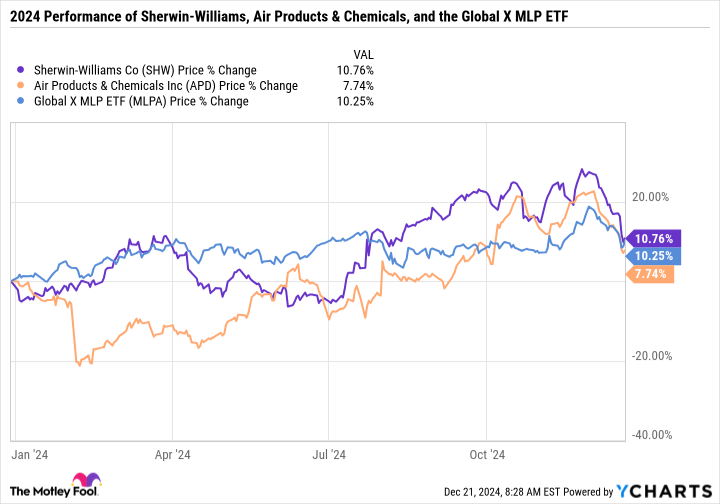

Sherwin-Williams (SHW 0.49%), Air Products and Chemicals (APD 0.84%), and the Global X MLP ETF (MLPA 1.32%) are up between 8% and 11% year to date. Three Motley Fool contributors offer up some fact-based arguments as to why these two dividend stocks and this ETF have more room to run in 2025 and beyond.

Image source: Getty Images.

Sherwin-Williams is at the top of its game

Daniel Foelber (Sherwin-Williams): It’s been another solid year for residential, commercial, and industrial paint and coatings supplier Sherwin-Williams. The stock is trading up over 10% year to date, even after undergoing a significant pullback in December.

Data by YCharts.

In November, Sherwin-Williams and Nvidia were added to the Dow Jones Industrial Average. The inclusion is a testament to Sherwin-Williams’ industry-leading position and the strength of its growing business.

Sherwin-Williams has delivered blowout gains for long-term investors, with the stock handily crushing the S&P 500 over the last decade. And there’s reason to believe that Sherwin-Williams can continue rewarding patient investors for years to come.

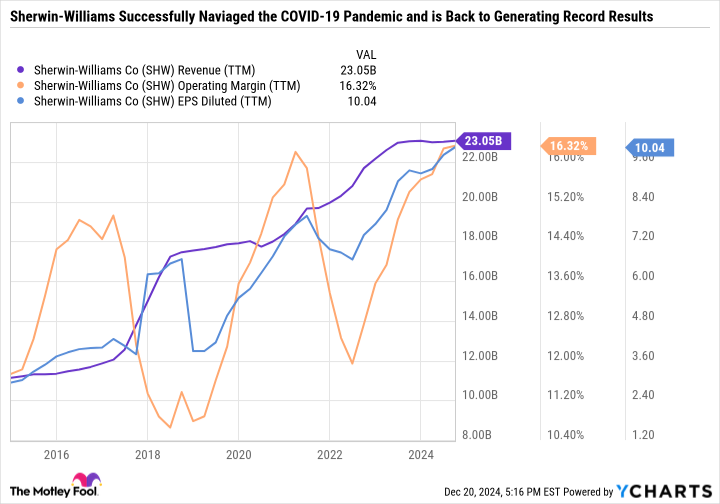

Sherwin-Williams did a masterful job of navigating the COVID-19 pandemic and has built upon that growth in recent years. As you can see in the following chart, Sherwin-Williams’ revenue and operating margin initially surged in response to an uptick in do-it-yourself (DIY) home improvement projects, which offset weakness in its industrial and commercial segments.

Data by YCharts.

However, the spike in demand proved to be short-lived, and Sherwin-Williams’ margins and earnings took a hit. But unlike many other DIY companies, Sherwin-Williams recovered quickly, and it is now generating all-time-high earnings, 10-year-high margins, and near-record-high sales.

For full-year 2024, revenue and earnings growth is expected to be fairly moderate, and there’s definitely a concern that higher interest rates could slow down economic growth and affect Sherwin-Williams. However, the company continues to do an excellent job with what it can control, which is expanding its portfolio of brands and leveraging its global supply chain and distribution network.

Sherwin-Williams only yields 0.8% because its stock price has significantly outpaced its dividend growth rate, but the company remains highly committed to growing its payout. In February, Sherwin-Williams announced a whopping 18.2% increase in its dividend, marking the 45th consecutive annual raise — putting the company on track to become a Dividend King by 2029. Add it all up, and Sherwin-Williams stands out as a quality company to buy now.

The burgeoning hydrogen economy is one reason for picking up Air Products stock

Scott Levine (Air Products): Air Products has seen its stock rise about 8% over the past year. Yet it’s still attractively priced and would make an excellent addition to income investors’ portfolios with its 2.4% forward-dividend yield. The company produces and distributes industrial gases to various industries, from food and beverage to energy.

Hiking its distribution higher for more than 40 consecutive years, the company finds itself among an elite group of dividend-paying stocks that have committed to steadily increasing their distributions for decades. Over the past decade, Air Products has raised its dividend payout at a 9% compound annual growth rate. But that’s hardly the only reason those looking to fortify their passive income streams would find Air Products stock appealing. For one, it consistently generates strong cash flow, illustrating the sustainable nature of its payout.

The conservative payout ratio indicates that the company isn’t jeopardizing its financial well-being to satisfy dividend-hungry investors. Over the past five years, Air Products has averaged a conservative payout ratio of 62%, leaving it well-positioned to continue investing profits back into the business.

Hydrogen, for example, is one area in which the company is committed to expanding its presence. Recognizing hydrogen as a trillion-dollar market opportunity, Air Products has already emerged as an industry leader and is working to further its position with projects such as the NEOM green hydrogen project. When it commences operations (presumably in late 2026), it will be the largest green hydrogen project in the world, with a daily production capacity of 600 metric tons.

There’s a new reality around the importance of natural gas in the economy

Lee Samaha (Global X MLP ETF): This ETF currently holds 20 master limited partnership (MLP) stocks. They are midstream pipeline and storage companies that tend to generate revenue on a long-term contract basis and can pay superior dividends to investors because they don’t pay corporate taxes.

Three factors changed in the natural gas pipeline and storage world in 2024, all favorable to this ETF. First, there’s an emerging reality that, although the clean energy transition is still taking place, it will not quite be at the pace many expected. As such, it’s clear that hydrocarbons, and notably natural gas, will play a major part in the energy mix for decades to come.

Second, the burgeoning demand for power from artificial intelligence (AI) applications is increasing expectations for electricity demand in the future, and that means more pressure on electricity networks and power demand, and in turn, fuel sources such as oil and gas.

Third, the U.S. presidential election result will usher in a more fossil-fuel-friendly administration. Whereas the Biden administration paused pending approvals of liquified natural gas (LNG) exports, President-elect Trump has promised to approve terminals on his first day back in office. Trump is reportedly drafting packages to support U.S. energy production.

All three of these events are likely to be lasting, and the recent dip in the ETF provides investors with a good entry point into a stock currently yielding more than 7%.

{kind=link}