Markets are stumbling following another hot inflation report. This morning’s Producer Price Index (PPI) soared past expectations and is reminding traders of the pain associated with last Tuesday’s Consumer Price Index. Indeed, this report has aligned the Fed’s projected rate path with the market’s as investors are now pricing in just three cuts this year; earlier this year, they expected seven. The sharp adjustment in expectations has yet to effect equities in a meaningful way, however, with bullish sentiment and better-than-expected earnings reports providing robust support. Equities are near the flatline as bonds selloff, but that’s not the only bifurcation today with consumer sentiment sustaining its bounce while construction activity takes another plunge.

Services Continue to Boost Prices

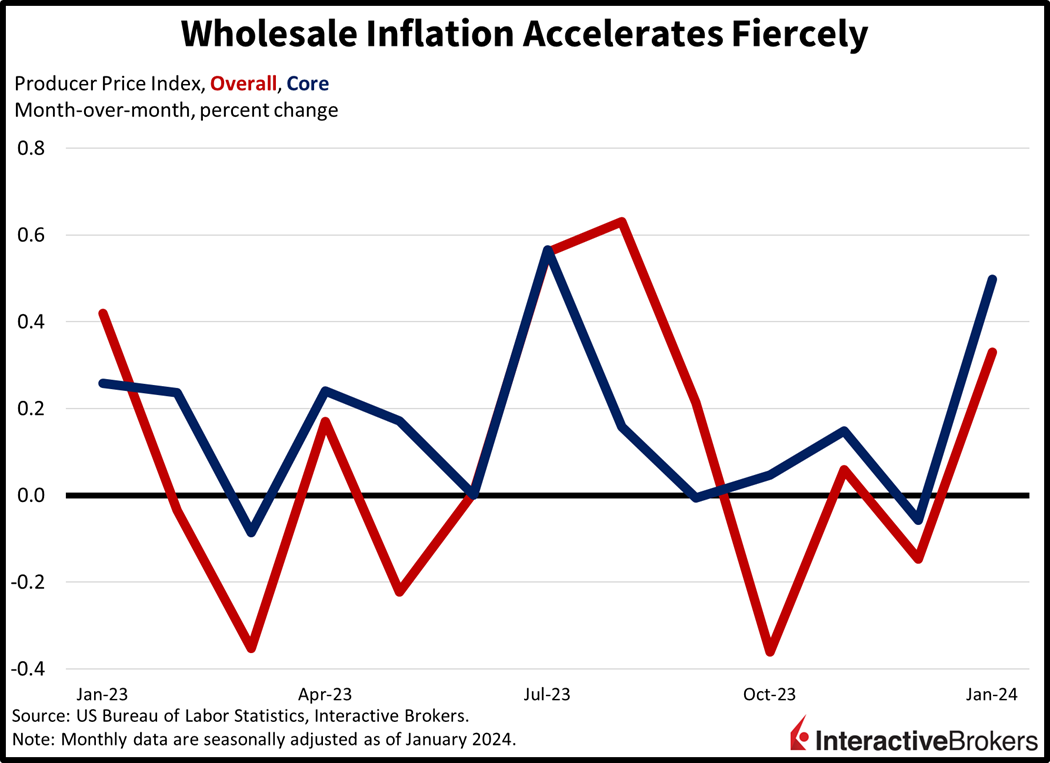

Wholesale prices rose sharply last month as the integral services sector kept the pressure on inflation. January’s PPI rose 0.3% month over month (m/m), much faster than the forecasted 0.1% and December’s 0.1% decline. The Core PPI, which excludes food and energy, rose a staggering 0.5% m/m, also stronger than the projected 0.1% and the previous period’s -0.1%. Year-over-year (y/y) figures came in at 0.9% for headline and 2% for core, a tenth of a percent softer for the former and three tenths higher for the latter relative to December.

The strength in this morning’s report was narrow, with goods and commodities providing firm downside pressure. Wholesale prices for goods, foods and energy fell 0.2%, 0.3% and 1.7% m/m. Costs for gasoline, electric power, hay, oil seeds, beef, veal, ethanol, iron and steel scrap led the charge lower. Services, meanwhile, rose a sharp 0.6% m/m, the fastest speed since July of last year. Hospital outpatient care, which rose a sharp 2.2%, led the price increases within the services category. Machinery and chemicals wholesaling, portfolio management, travel accommodation and legal services also contributed to the upward push.

Affordability Weighs on Real Estate

In real estate land, construction activity dipped sharply in January against the backdrop of severe affordability headwinds. Higher mortgage rates continue to widen the gap between seller and buyer negotiations. On the one hand, sellers want to transact at lofty prices to offset inflationary pressures in the economy and to capture enough equity to avoid buying elsewhere with a much higher mortgage rate. Buyers are sidelined though, as incomes and monthly mortgage payments remain acutely out of whack. In the multifamily sector, landlord margins are disappearing as tenants aren’t able to absorb rent increases and have many options for finding lower-cost housing, a result of buoyant apartment construction in recent years. Furthermore, higher interest expenses and rising costs for insurance, maintenance, materials and labor are weighing on bottom lines.

Homebuilders slowed activity last month on fears that buyers won’t show up post-construction. The pace of housing starts and building permits dipped 14.8% and 1.5% to 1.331 million and 1.470 million seasonally adjusted annualized units (SAAU). The figure missed estimates of 1.46 million and 1.509 million SAAU. The weakness was primarily driven by the multifamily segment, which fell 35.8% and 9% m/m for starts and permits. Starts fell in all four regions, with the Midwest, Northeast, West and South experiencing declines of 30%, 20.6%, 15.7% and 9.7% m/m. Permits were positive in all regions except the most active one, as the pace declined 7% in the South. The Northeast, Midwest, and West rose 19.4%, 6.6% and 1.5%.

Consumer Sentiment Remains Positive

Consumer sentiment remained favorable this month, as households were optimistic regarding job opportunities, the path of disinflation and business possibilities. The University of Michigan’s Consumer Sentiment level of 79.6 nearly matched the anticipated 80 while improving slightly from last month’s 79. Indices for current conditions and consumer expectations arrived at 78.4 and 81.5, with the former improving from 77.1 while the latter lost marginal ground, slipping slightly from 81.9. Inflation expectations rose modestly, with one-year projections rising from 2.9% to 3% while the five-year figure remained unchanged at 2.9%.

China Snaps Up Semiconductor Equipment as US Consumers Weaken

Semiconductor providers in China and elsewhere are rushing to buy manufacturing equipment as internet-connected devices are increasing demand for computer chips. Consumers, however, are tightening their purse strings by scaling back on streaming entertainment. The following earnings highlights illustrate these trends:

- Applied Materials, a provider of semiconductor manufacturing equipment, posted strong quarterly results, including sales growth in China, which sparked optimism that the industry is gearing up to increase production. Additionally, the company’s guidance exceeded expectations, causing its share price to surge more than 11% in extended trading. Applied Materials reported earnings per share (EPS) of $2.13 after adjusting for one-time expenses. The EPS climbed 5% y/y and surpassed the analyst expectation of $1.90. The increase resulted from the company managing its expenses and occurred even with the company’s quarterly revenue of $6.71 billion, which beat the analyst expectation of $6.48 billion. Revenue was nearly flat y/y with a marginal $32 million decline. Sales in China totaled $3 billion, more than doubling y/y despite the country suffering from declining export orders, a languishing real estate sector and weakening gross domestic product growth. In a Bloomberg interview, Applied Materials Chief Executive Officer Gary Dickerson said overall demand for semiconductors is being driven by the increasing types of devices that have computer chips and the increase in the number of chips per device, with some cars having thousands of chips. Applied Materials estimates current-quarter sales will reach approximately $6.5 billion, significantly above the analyst expectation of $6.32 billion. The company also estimates its adjusted EPS will range from $1.79 to $2.15, while analysts expected guidance at the lower end of that range.

- Roku shares dropped more than 17% after the company reported a larger-than-expected loss. For the recent quarter, the company’s loss of $0.55 per share was worse than the $0.52 loss expected by analysts but much better than the $1.70 loss in the year-ago quarter. The company’s $984.4 million in revenue, however, exceeded the analyst expectation of $959.6 million and climbed from $867 million y/y. Roku also increased its number of active accounts 14% to 80 million while streaming hours of content increased 21% to 29.1 billion. In a sign of weakening consumer spending, however, existing customers spent less on Roku options with the average revenue per user declining 4% y/y to $39.92. The company expects first-quarter revenue to reach $850 million while analysts expected guidance of $834.1 million. The guidance failed to offset the impact upon Roku’s share price of the larger-than-expected quarterly loss and recent news that Walmart may acquire smart television manufacturer Vizio.

Inflation Fears Spark Selloff

Investors are selling stocks and bonds this session as they factor in the risk of a continued acceleration in price pressures. The downside charge is being led by the small-cap, cyclically tilted Russell 2000 Index; it’s down 0.7%. The Nasdaq Composite, Dow Jones Industrial and S&P 500 benchmarks are down a milder 0.2%, 0.2% and 0.1%. Sector breadth is mixed, with four out of eleven sectors higher while four other ones are down but near the flatline. Leading the decline are the communication services, real estate and consumer discretionary segments, which are down 1%, 0.7% and 0.2%. Materials, health care and energy are leading with gains of 1%, 0.7% and 0.2%. Rates are jumping with the 2- and 10-year Treasury maturities trading at 4.68% and 4.31%, 10 and 7 basis points (bps) higher on the session. The dollar is gaining slightly as higher rates provide support. The greenback’s index is up 4 bps to 104.31 as the US currency gains against the euro, pound sterling, franc, yen, yuan and Canadian dollar. It is down relative to the Aussie dollar though. Crude oil is higher on continued tension in the Middle East, with the WTI benchmark up $0.27, or 0.4% to $77.80 per barrel.

A Bad Week for Price Stability

The Fed has sought to dampen investor optimism for potential spring rate cuts by emphasizing that it needs more evidence that price stability improvements are durable and that a shift to accommodative monetary policy won’t spark a resurgence in inflation. To that end, this week is a setback, with CPI data depicting stronger-than-expected January inflation and today’s PPI showing that wholesalers jacked up prices during the same month. Future data could also depict inflation being persistent rather than this week being an isolated setback. Prices for services, goods and gasoline have all climbed this month, while in January, the inflation-sticky services category was the only culprit that propelled the indices higher. In my view, this week’s CPI and PPI data may rule out a June rate cut while certain policymakers have expressed renewed expectations for delaying a dovish shift. Last night, Atlanta Fed President Raphael Bostic said rate cuts are unlikely until the third quarter of this year. With recent market gains being driven by valuation expansion resulting from optimism of spring rate cuts, the persistence of inflation is likely to drive a considerable realignment in short order.

Visit Traders’ Academy to Learn More About Consumer Sentiment and Other Economic Indicators.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Forex

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

{kind=link}