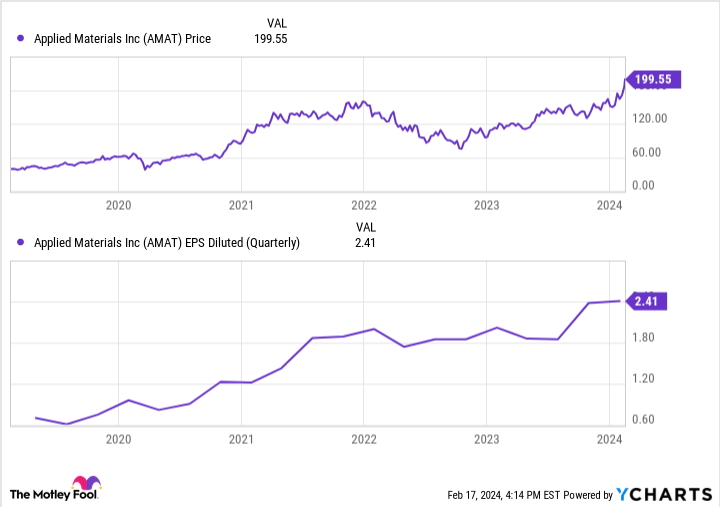

The stock of leading semiconductor equipment supplier Applied Materials (AMAT 6.35%) rallied 6.4% on Friday to all-time closing highs near $200, following the company’s first fiscal quarter earnings report.

As I’ve written before, Applied is one of the least-risky ways to play the growth of semiconductors and artificial intelligence applications. But is the stock still a buy at all-time highs?

A diversified “arms dealer” to semis and AI

While Applied is known by many as a very cyclical stock, it has actually proven less cyclical than investors may have feared during the post-pandemic downturn.

Applied is the most diversified semiconductor equipment supplier, with a concentration in crucial etch and deposition manufacturing steps, along with metrology, inspection, and packaging equipment as well.

The diversity has a lot of advantages, which were on display over the past year. In spite of a rather nasty downturn in the memory and leading-edge chips, Applied was able to maintain a fairly healthy earnings per share through all of 2022 and 2023, with only a flattening of earnings and not a big decline like some other peers experienced.

Needless to say, the stock’s 50% or so drop in 2022 didn’t seem to jive with what ultimately were fairly mild profits declines. And with profits now basing and beginning to turn up, no wonder investors are growing optimistic.

Revenue went down, but the stock skyrocketed?

At first glance, it may not seem like Applied should have gone up so much after earnings. After all, during the fiscal fourth quarter, revenue slightly declined. But the final figure of $6.71 billion beat expectations by $221 million. Moreover, adjusted (non-GAAP) earnings per share actually increased by 5%, thanks to Applied maintaining margins and continuing to buy back a healthy amount of stock.

While Applied only guided for $6.5 billion in revenue next quarter – again, a small decline – that was also ahead of analyst expectations of $6.3 billion. And Applied usually guides conservatively, so it’s likely the company beats that number and may even grow quarter-over-quarter.

So why would the stock go up so much? Well, semiconductor investors tend to buy stocks once they believe earnings are “troughing” and getting ready to turn up. With the PC and smartphone post-pandemic “bust” showing signs of recovery and the AI revolution kicking in, investors are growing optimistic about a semiconductor recovery and therefore chip equipment spending later in 2024.

While today’s valuation at 23 times earnings may seem somewhat steep, remember those are near-bottom-of-the-cycle trailing numbers.

The market believes in Applied’s “inflections”

Besides a general semiconductor recovery, Applied touted its leadership in several key technology “inflections” that should give it outsized market share growth on top of that.

The first inflection is a new transistor structure called gate-all-around (GAA). This is an entirely new way to build transistors on a chip, which will now be surrounded on all four sides by the control gate. The tighter control over the transistor should result in a 30% increase in a chip’s energy efficiency, according to management.

A second new invention is something called backside power, whereby the power controls on a semiconductor are built on the back of the chip, freeing up more space on the die for more transistors, making the chip more powerful. The switch of backside power should yield another 30% increase in transistors per chip, even with no node shrinking.

And a final tech inflection is advanced packaging, whereby chips, high-bandwidth memory, and even parts of chips called “chiplets” are fused together in new and novel ways to boost power and efficiency.

Applied says it’s is pulling ahead of competitors in all of these inflections, thanks to its broad exposure and ability to see around corners, while also making co-optimized solutions.

Management says the GAA transition will increase Applied’s opportunity by $1 billion for every 100,000 wafer starts per month. Moreover, management says it’s poised to gain market share on the GAA transition, taking over 50% of total equipment spending on GAA chips.

The overall foundry industry is set to hit about 10 million wspm in 2024. While gate-all-around is only going to be produced on the most leading-edge slice of that market, one can see how the market can grow over time. And even a 5% proportion going to GAA chips, or 500,000 wspm, would yield a significant $5 billion opportunity for Applied.

Applied also says it’s gaining share in high-bandwidth memory (HBM), after having gained about 10 points of market share in DRAM spending over the past decade. Of note, HBM is a crucial bottleneck in the AI ecosystem and is forecast for very strong growth in 2024. And Applied believes its packaging equipment for HBM will quadruple in 2024 alone, albeit off a small base.

In short, Applied is gaining share in major growth areas

Applied’s wide exposure to various parts of the industry have allowed it to anticipate major trends and also combine technologies together that other specialists might not be able to achieve.

So not only are semiconductors beginning their current up-cycle, but Applied Materials also stands to gain market share on top of that. At a mere 23 times bottom-of-the-cycle earnings, which is just a market multiple, Applied actually doesn’t look that expensive despite the stock achieving all-time highs.

With an AI boom in its early stages, Applied should be a core tech holding and still looks like a buy, believe it or not.

{kind=link}