Key takeaways

Is it time for international stocks?

The US dollar appears to have peaked and leading economic indicators in the developed world appear to have stabilized.

Is it time for small caps?

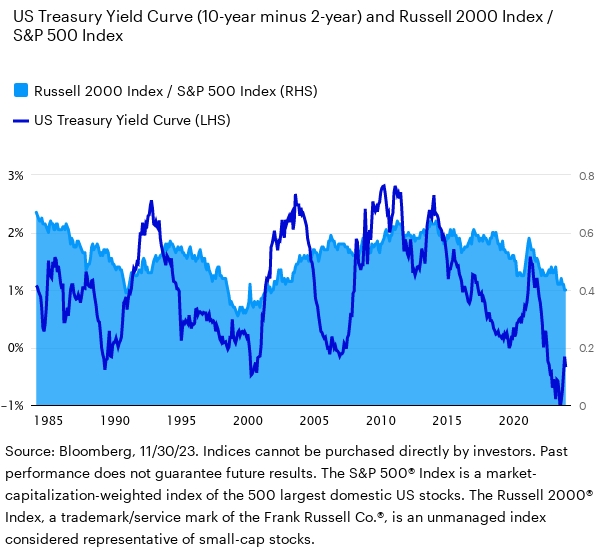

Small-cap stocks have tended to outperform large-caps as the US Treasury yield curve has normalized.

It’s always time for family.

The new year is a great time to gather the family together to assess finances and ensure everyone is prepared for the future.

It’s the holiday season, so hoop-de-do. My apologies, but if I need to have Andy Williams stuck in my head for a month then so do you. It does feel apropos to have the song on repeat in my mind given the state of the US economy. The merry bells are ringing with inflation coming down rapidly1 and the economy remaining resilient. This cycle, like all cycles, will end — but that ending isn’t imminent. It appears, at least for now, that the trip down the chimney will be a soft one. My hope is that this will mean goodies for you and me and other investors.

Brevity isn’t my strong suit, but I’ve promised to keep it short this month. My editors and compliance officers deserve a lighter workload during the holiday season…holiday season, so hoop-de-do and dickory dock. Please make it stop!

How did we do?

At this time last year, I confessed that the FOMO — fear of missing out — that I feel about social situations had made its way into my investing life as well. I had read many of the bearish 2023 outlooks and listened to the recession fears, but personally put a lot of emphasis on the fact that markets have typically performed well in the years after inflation had peaked.2 I didn’t want to miss it even if near-term challenges emerged.

Alas, my FOMO confession didn’t score me better invites to New Year’s Eve parties (I was quite happy in my neighbor’s basement), but it did have me on the right side of markets in 2023.

Resolutions are never broken

I am resolved to resume those family meetings that I am always preaching about in my financial literacy presentations. Truth be told, those meetings are too few and too far between in our family. It’s a classic case of “do as I say, not as I do.”

The new year is a great time to gather multiple generations of the family together. Think of it like an earnings call. Affirm the values and purpose of the entity, assess financial situations, consider strategic investments, and ensure that everyone is prepared for what will or could come next. If possible, keep the airing of grievances to a minimum!

It may be confirmation bias but…

…the job market has been cooling at a market-friendly pace and is appeasing the US Federal Reserve. Remember those 12 million unfilled jobs without enough people to fill them?3 The fear was that businesses would feverishly compete to fill them, resulting in a wage-price spiral the likes of which the US hasn’t experienced since the 1970s. The number of open jobs is now coming down, even as the US unemployment rate remains historically low.4

The reality is that we were never going to fill each of those jobs. The positions were opened during a period of outsized economic growth that wasn’t sustainable. A moderating jobs market is precisely what the Fed has been hoping to see.

Since you asked

Here’s a question I’ve been getting lately:

Q: What would it take for you to consider diverting money from US equities and putting it in international equities?

A: For me, it would take the type of environment that we appear to be in now. For one, the US dollar appears to have peaked5, which is often the case following the end of monetary policy tightening. And two, leading economic indicators in the developed world appear to have stabilized and are turning upward from a depressed level.6 We view those as two important catalysts to potentially unlock some of the value that we see in international markets.

It was said

“What a difference a month can make.” – Randall W. Forsyth, Associate Editor at Barron’s.

November was the biggest one-month rally in the US Treasury market since the early 1980s, not coincidentally the last time the US Federal Reserve worked feverishly to contain inflation.7 Nonetheless, there is still $5.9 trillion in money market assets.8 I understand. Short-term Treasury yields appear attractive, but they may not be there forever. The moves in the Treasury market in November will hopefully serve as a wake-up call that moving out on the Treasury yield curve can help lock in the yields for a long-term investment horizon.

Automate my job?

Each month I pose a question to ChatGPT — the artificial intelligence-driven chatbot — and assess the response.

Q: What asset classes perform well as the US Treasury yield curve normalizes?

A: As the yield curve normalizes, historically, sectors like financials tend to perform well. Additionally, value stocks may outperform growth stocks in such periods. It’s important to consider a diversified approach based on your risk tolerance and investment goals.

That’s a reasonably good answer — ChatGPT must have picked up on the Bloomberg data showing that, from 1989 to today, S&P 500 financials companies have also tended to outperform S&P 500 technology companies when the yield curve steepened. (It’s learning!). I would add that small-cap stocks have tended to outperform large-cap stocks as the yield curve has normalized.9 In the chart below, the higher the dark blue line, the steeper the yield curve (below 0% representing an inverted yield curve). And the higher the light blue area, the greater the small cap outperformance over large caps.

Small caps have tended to outperform as the yield curve has steepened

Everyone has a podcast

Kristina Hooper, Chief Global Market Strategist and Alessio de Longis, Head of Investments for Invesco Investment Solutions, returned to the Greater Possibilities podcast to discuss their outlooks for 2024.

On the road again

I traveled to Philadelphia to celebrate the retirement of a close friend and long-time colleague. If you measure success as the friends you have made and the respect that you have earned, then our retiree was a resounding success. Colleagues came from around the country to raise a glass in his honor. I was overwhelmed by the emotion in the room. That it took place in the city of brotherly (and sisterly) love was not lost on me.

One of our colleagues, Ian Roche, drove from Cleveland to Philadelphia to be at the celebration. That’s 13 hours roundtrip. When I showed my surprise at the lengths he took to be there, he told me that he wouldn’t have missed it for anything. I said, “and that’s why we all love you.” Two weeks later I received the crushing news that Ian had died unexpectedly at the age of 56. I feel like I lost a family member. In many ways I have. We come to work to earn a living. Some even find a calling. The luckiest ones gain a new family. Rest in peace my work brother.

Let’s remember to reflect this holiday season on what matters most. I wish everyone a happy and healthy holiday season. I’ll see you in 2024.

Footnotes

- Source: Bureau of Labor Statistics, 10/31/23. Based on the US Consumer Price Index.

- Source: Bloomberg and Bureau of Labor Statistics, 12/31/22. Based on the performance of the S&P 500 Index in the 1-, 2-, and 3-year following previous inflation peaks: Feb. 1970, Dec. 1974, Mar. 1980, Dec. 1990, and Jul. 2008

- Source: Bureau of Labor Statistics, 11/30/23. Represented by the US Job Openings by Industry total, which peaked at 12 million in March 2022.

- Source: Bureau of Labor Statistics, 11/30/23. Represented by the US Job Openings by Industry total.

- Source: Bloomberg, 12/7/23. Based on the US Dollar Index, which measures the US dollar versus a trade-weighted basket of currencies.

- Sources: Bloomberg L.P., MSCI, FTSE, Barclays, JPMorgan, Invesco Solutions research and calculations, from 1/1/92 to 11/30/23. The Global Leading Economic Indicator (LEI) is a proprietary, forward-looking measure of the growth level in the economy.

- Source: Bloomberg, 11/30/23. Based on the performance of the Bloomberg US Treasury Index, which returned 3.47% for the month.

- Source: Investment Company Institute, 12/6/23.

- Source: Bloomberg, 11/30/23. The yield curve is defined as the difference between the 10-year US Treasury rate and the 2-year US Treasury rate. Based on the performance of the Russell 2000 Index compared to the S&P 500 Index.

—

Originally Posted December 18, 2023 – Above the Noise: Anticipating a new year and a new market environment

Important information

NA3280534

Investors should consult a financial professional before making any investment decisions. This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

All investing involves risk, including the risk of loss.

Past performance does not guarantee future results.

Investments cannot be made directly in an index.

Diversification does not guarantee a profit or eliminate the risk of loss.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Stocks of small and mid-sized companies tend to be more vulnerable to adverse developments, may be more volatile, and may be illiquid or restricted as to resale.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

The profitability of businesses in the financial services sector depends on the availability and cost of money and may fluctuate significantly in response to changes in government regulation, interest rates and general economic conditions. These businesses often operate with substantial financial leverage.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Tightening monetary policy includes actions by a central bank to curb inflation.

The yield curve plots interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates to project future interest rate changes and economic activity. An inverted yield curve is one in which shorter-term bonds have a higher yield than longer-term bonds of the same credit quality. In a normal yield curve, longer-term bonds have a higher yield.

The US Consumer Price Index (CPI) measures change in consumer prices as determined by the US Bureau of Labor Statistics. Core CPI excludes food and energy prices while headline CPI includes them.

The Bloomberg US Treasury Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. The US Dollar Index measures the value of the US dollar relative to majority of its most significant trading partners.

The opinions referenced above are those of the author as of Dec. 12, 2023. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Disclosure: Invesco US

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2022 Invesco Ltd. All rights reserved.

Before investing, carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}