Market participants are dealing with economic cross currents this morning, sparking wild swings between gains and losses. The first stateside economic report from ADP depicted the slowest job growth since early 2021, which resulted in equity prices slipping. But unemployment claims and ISM-Services prints, released 15 and 105 minutes later, provided stock bulls with a boost, due to the stronger-than-anticipated results relieving investors of fears of an imminent recession. Still, tomorrow’s nonfarm payrolls is expected to be a big market mover, with a large miss or sizable beat likely to help the bears as it’ll point to either a slow and controlled vertical walk down the monetary policy stairs or a speedy and disorderly horizontal roll to lower stories. Meanwhile, a number in-line with estimates can be open to interpretation and is likely to offer neutrality for bulls and bears alike.

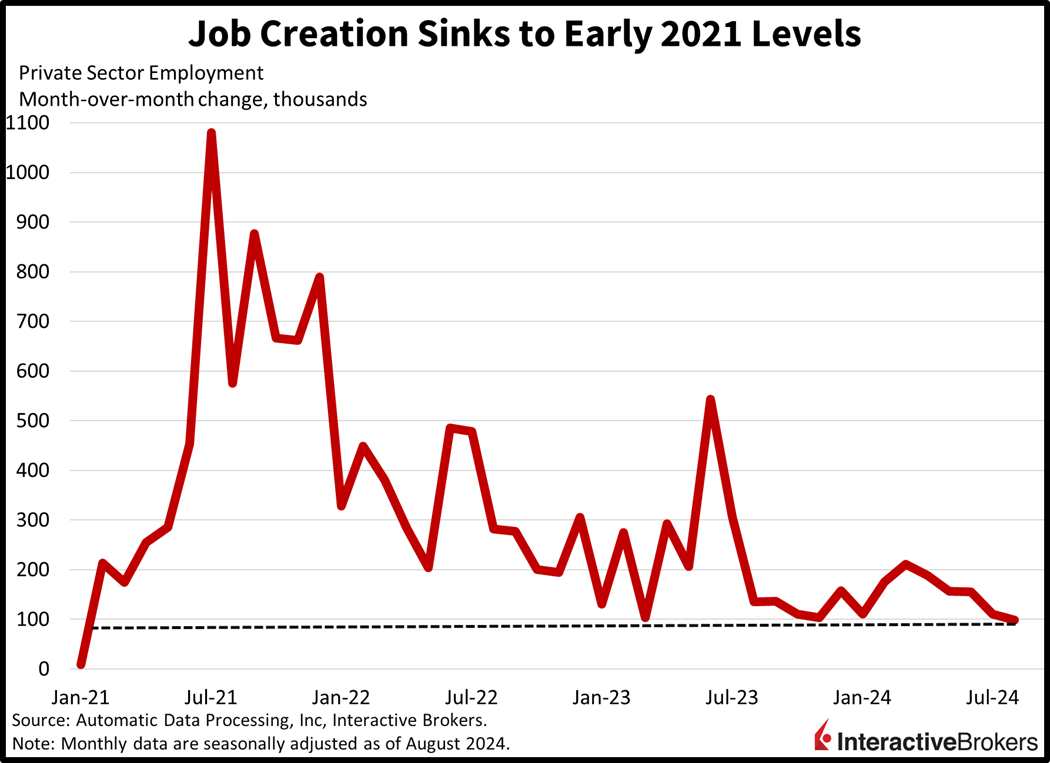

Employers Back Off Gas Pedal

Hiring conditions decelerated meaningfully last month as corporations navigated uncertainties related to profitability outlooks, the upcoming presidential election and monetary policy. The private sector added 99,000 jobs, well beneath projections of 144,000 and July’s 111,000, according to ADP. The following size firms added/lost the stated number of positions:

- Small, – 9,000

- Mid, 68,000

- Large, 42,000

Among industries, the education and health services category led hirings with 29,000 positions filled. Other gainers and the number of hires were as follows:

- Construction, 27,000

- Other services, 20,000

- Financial activities, 18,000

- Trade, transportation and utilities, 14,000

- Natural resources and mining, 8,000

Professional and business services surrendered the most jobs with the total headcount slashed by 16,000, followed by manufacturing, which shed 8,000 workers and information, with 4,000 fewer employees. In another sign of labor market cooling, compensation pressures softened, with the year over year (y/y) wage increases for job changers and job stayers dropping from 7.7% and 4.9% to 7.2% and 4.8%.

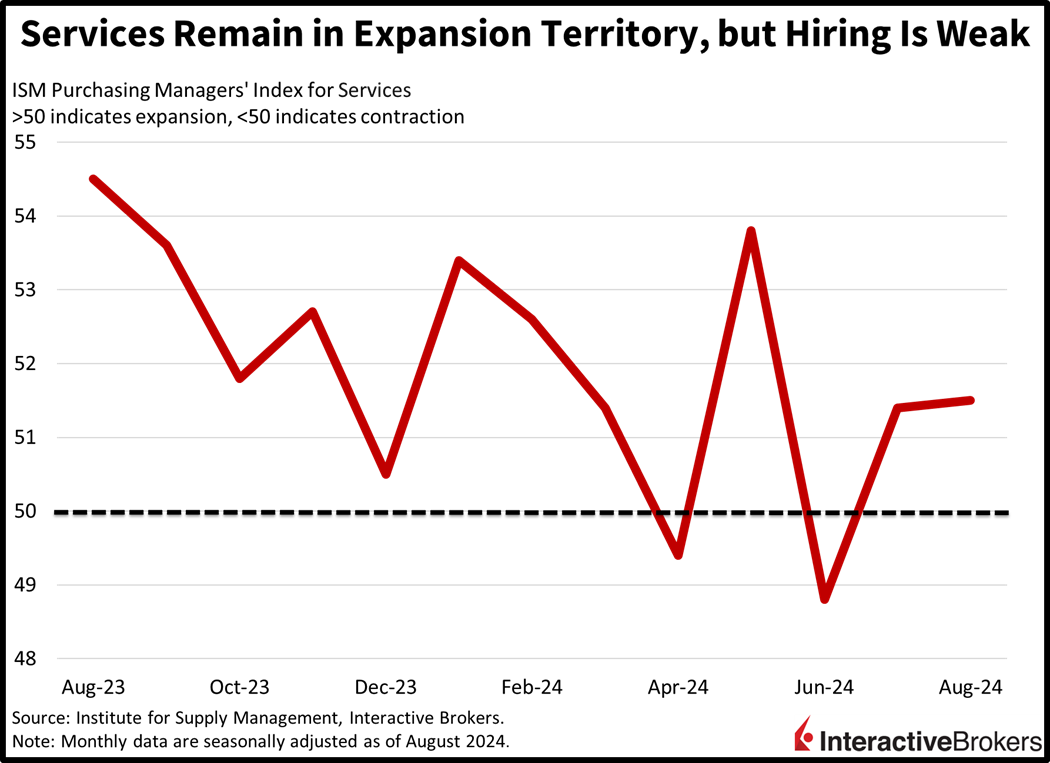

Services Activity Picks Up

Despite slowing headcount additions, the Purchasing Managers’ Index for Services from the Institute for Supply Management (ISM) depicted accelerating economic growth. August’s figure of 55.7 was firmer than the median estimate of 55.2 and July’s 55. Driving the upside beat were prices, business activity and orders, which arrived at 57.3, 53.3 and 53, well above the expansion-contraction threshold of 50. But employment barely expanded, sporting a score of 50.2. This report is confirming what we’re seeing from other employment reports—sure, employers aren’t firing much, but they aren’t hiring either. Also, we’re seeing that demand increases are being accompanied by price pressures, which is a dynamic the Fed doesn’t want to see.

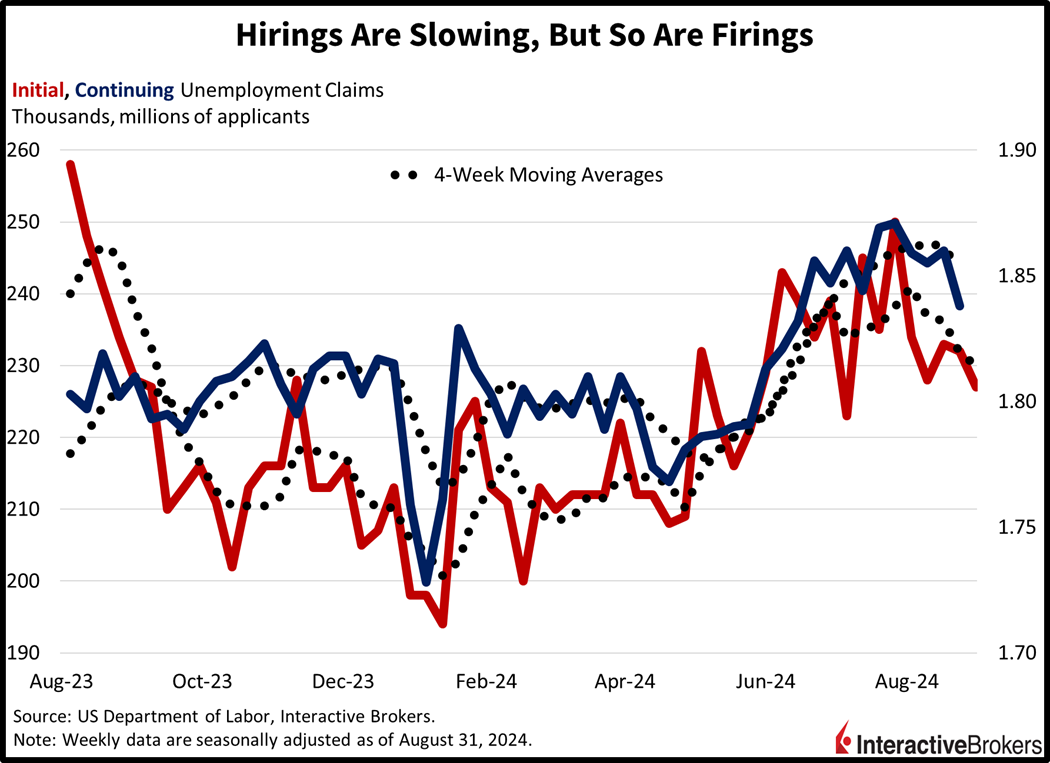

Firings Moderate Slightly

Unemployment claims ticked lower in the last two weeks, pointing to employers looking to do more with less rather than enacting wide-scale roster reductions. Initial claims declined to 227,000 for the week ended August 31, below estimates of 231,000 and the previous week’s 232,000. Similarly, continuing claims dropped to 1.838 million during the week ended August 24, under the 1.860 million for the prior period and the 1.870 million expected. Four-week moving average trends did move south on both fronts, from 231,750 and 1.861 million to 230,000 and 1.853 million.

Global Recruiter Experiences Decline in Search Demand

At least one large employee-recruiting firm has noted weakening demand for its services, while in the tech sector, artificial intelligence is continuing to help hardware shops grow their revenues. In the retail sector, some homeowners may be spending more time playing golf than maintaining their lawns as sales of mowers and related equipment have declined. Those are a few observations from the following earnings highlights:

- Korn Ferry (KFY), an organizational consultant, reported weakening demand for employee recruiting services but still posted better-than-anticipated results for revenue and earnings during the fiscal quarter ended July. The company’s executive search fee revenue climbed 2% y/y while its consulting and digital segments were flat. KFY stock fell approximately 3.3% in response to the company providing a mixed view of the current quarter. The middle of its projected earnings per share (EPS) range met the analyst consensus expectation while revenue guidance fell below Wall Street’s outlook.

- Hewlett Packard Enterprise (HPE) reported a 39% quarter-to-quarter increase in revenue from AI enabled servers, underscoring strong demand for systems that can facilitate the technology. The company ended the recent quarter with a $3.4 billion order backlog. However, the increased portion of sales resulting from less profitable AI-products and high input costs, such as AI-capable semiconductors and materials for solid state drives, contributed to the company’s gross margin ratio declining and missing analyst consensus expectations, which triggered a 3% decline in HPE’s price. On a positive note, total revenue climbed 10%. The metric, along with the company’s EPS, exceeded analyst expectations. Additionally, HPE President Antonio Neri noted that sales of AI servers are not cannibalizing sales of other types of equipment.

- Toro (TTC) reported earnings and revenue that missed analyst expectations, causing its share price to drop approximately 13% in early trading. Macro uncertainties weighed upon sales of residential lawn equipment; however, the company has scaled back its inventory of mowers and other related equipment at dealers. During the recent quarter, commercial products for golf courses and infrastructure projects were bright spots that experienced strong demand. Based on the volume of golf rounds being played, the company expects fairway equipment sales to remain robust. It is also optimistic about its infrastructure equipment. Nevertheless, Toro lowered its full-year guidance. Adjusted EPS is now projected to range from $4.15 to $4.20. Analysts anticipated guidance of $4.31. Toro also said it anticipates full-year revenue to increase only 1%.

Confusion Runs Rampant Through Markets

Markets are now getting pounded by widespread confusion concerning hirings, layoffs, price pressures, seasonal headwinds and more. Bears digested the ISM-services print faster than everyone else. It pointed to a stalling labor market despite strong beats for the headline and new orders. All major equity indices are trading south with the Dow Jones Industrial, Russell 2000, S&P 500 and Nasdaq Composite lower by 0.9%, 0.9%, 0.6% and 0.2%. Sectoral breadth is awful with every segment retreating except for consumer discretionary, which is gaining 0.6%. Piloting stocks to the basement are healthcare, industrials and financials, which are losing 1.7%, 1.6% and 1.3%. Treasurys are once again nearing that pivotal de-inversion across the 2- and 10-year maturities, which are changing hands at 3.756% and 3.748%, flat on the session. The dollar is also unchanged as it awaits tomorrow’s big Jobs Friday. The US currency is appreciating relative to the franc and Aussie and Canadian dollars but is depreciating versus the euro, pound sterling, yen and yuan. Commodities are bullish, however, with lumber, silver, copper, gold and crude oil trading north by 3%, 2%, 1.2%, 0.6% and 0.5%. WTI crude is at $69.59 a barrel as OPEC+ decided to postpone its output increases for two months, hurting the supply outlook.

Next Year Could be a Flop

With recent data pointing to a softening job market and investors having high expectations for corporate earnings growth, next year could be disappointing. While some labor market metrics are looking fine at the moment, continued weakening could eventually dampen household spending and hurt overall revenues. The ability for businesses to cut operating costs or capture market share will therefore be crucial. With a forward P/E of 21, the S&P 500’s valuation exceeds both the 5- and 10- year averages by wide margins, illustrating that earnings growth will be essential in sustaining equity gains. But in the short term, tomorrow’s payroll data could lead to a firm de-inversion across the yield curve and generate painful equity selling. Ladies and gentlemen, I’m expecting 130,000 payroll additions, but Wall Street and IBKR Forecast Traders are more optimistic, with the former cohort projecting 164,000, while the latter market is pricing the over, or Yes contract, at $0.73 for a figure above 147,300. Personally, I like the no and defensive positioning in equities going into the report. Just remember, markets are like sports, and unexpected things can happen.

To learn more about Forecast Contracts, please view our recent podcast with Wall Street Veteran and ForecastEx CEO David Downey here.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ForecastEx

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx forecast contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

Disclosure: Forecast Contracts

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Hong Kong Limited, and Interactive Brokers Singapore Pte. Ltd.

{kind=link}