The Fed has been walking a tightrope for a while now, trying to tame inflation without crashing the economy. The data was encouraging throughout 2023, and we may soon find out if the central bank has actually engineered immaculate disinflation.

What a difference a year makes. Heading into 2023, the consensus view among economists was that a recession would occur within the next twelve months – an unprecedented level of certainty for an inherently hard to predict outcome. At the time, the debate simply revolved around whether the recession had already started or would begin in the next quarter or two. Inflation in the U.S. was still roaring at well over 6% in January, leading the Federal Reserve and other global central banks to continue tightening credit by rapidly raising interest rates. Then a rash of regional bank failures starting in March of 2023 seemed to represent the necessary catalyst for tipping the U.S. into recession.

Fast forward to January of 2024, and the situation has dramatically changed. The regional banking sector has stabilized with support from the federal government, while larger well-capitalized banks have seen little disruption in their businesses. Inflation has slowed dramatically to just 3% as of November. And as a result of decelerating inflation, the Fed signaled in December 2023 that rate hikes have paused — and in a particularly unexpected twist, the Fed stated that it expects as many as three rate cuts in 2024, a dramatic reversal coming on the heels of the fastest rate rise in over 40 years.

Perhaps the two most important factors that have enabled the economy to continue expanding despite all the volatility have been low unemployment and growing wages in excess of inflation. Unemployment in January 2023 was 3.4%, and it crept to 3.7% as of November 2023. This has meant that workers have remained gainfully employed at a very healthy rate, with only modest deterioration in the rate of unemployment. Meanwhile, real wages from November 2022 to November 2023 rose 1%, meaning workers actually increased their purchasing power over that timeframe despite the inflationary bout we have gone through.

This balanced combination of low unemployment and growth in real wages has allowed consumers to continue purchasing, and the magnitude of the wage growth has not catalyzed a dreaded wage-price spiral, whereby wages explode and force companies to raise prices aggressively in order to offset higher labor costs, leading to further wage hikes, etc. — an unpleasant potential outcome that seemed highly plausible twelve months ago.

If the U.S. truly avoids a recession in 2024 and inflation remains low at 2-3%, Jerome Powell has likely earned himself a legacy besting even that of Paul Volcker, who slayed the inflation dragon of the early 1980s but by inflicting significantly more economic pain on the U.S. economy as unemployment peaked at just under 11% in November 1982. The disinflation of 2023 indeed looks immaculate.

Persistently Narrow Market

Consistent with the broad economy looking healthy, despite certain sectors like regional banking facing significant pressure, our companies generally fared well in 2023. Idiosyncratic industry-specific headwinds hurt certain companies, while others faced difficulty dealing with elevated inflation, but overall our companies saw growing revenue and profits, and many achieved record levels of profitability in 2023.

In spite of this fact, gains in the stock market in 2023 remained unusually narrow, driven by the so-called Magnificent 7: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. Although the rally somewhat broadened later in the year, these seven companies accounted for roughly 60% of the returns in the S&P 500, an outsized impact for an incredibly thin slice of the index.

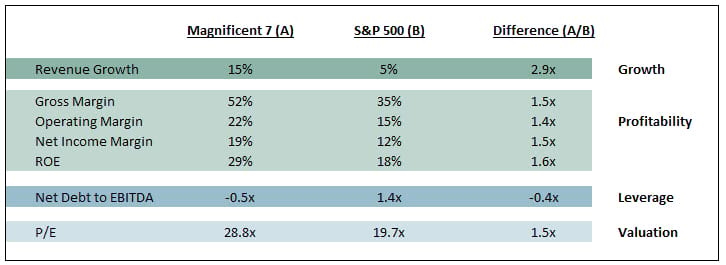

At first blush the narrow market gains seem like a textbook case of momentum investors crowding out fundamental investors. However, we believe there is some logic to the narrowness. In aggregate, the Magnificent 7 boast significantly better financial statistics than the broader S&P 500 — with roughly three times the revenue growth rate of the S&P 500, substantially higher profitability and returns on equity than the broad index, and cash well in excess of debt — a key advantage in a higher-interest rate environment. Consistent with superior financial metrics, several of the seven companies (including the three we own) enjoy extraordinary scale advantages, network effects, and secular tailwinds that should have the potential to protect growth and profitability for the foreseeable future.

Source: Bloomberg. Revenue growth reflects projections for 2024 vs. 2023 estimates.

The two caveats we would highlight, however, are that 1) the Magnificent 7 now trade at approximately 1.5x the broader S&P 500, and 2) we think that some of these companies appear particularly vulnerable to greater competition, slower growth, and lower profitability in the future. Premium valuations coupled with prospective deterioration in fundamentals create significant risk for stock price performance for at least some of these seven companies.

Furthermore, there is a long history of the S&P 500 market cap-weighted index outperforming the equal weighted index over relatively short time periods. But over longer periods, the indices have historically performed roughly in line.

In 2023, the market cap-weighted S&P 500 returned 27%, while the equal-weighted index returned 14%. In other words, had you owned a basket of all 500 companies in the index equally weighted, you would have earned roughly half of what you earned in the market cap-weighted index.

However, over the past 20 and 30 years, the market cap-weighted and equal-weighted indices both generated about 10% annualized returns. We think the longer-term convergence of market cap-weighted and equal-weighted returns will persist in the future, in large part because valuation is an important governor on stock price performance, even if fundamentals are exceptionally strong. And some of these seven companies will inevitably stumble, and perhaps even be dethroned. The seven largest components of the S&P 500 25 years ago were GE, Coca-Cola, Microsoft, Exxon, Intel, Merck, and Procter & Gamble. Only one — Microsoft — remains in the top seven today. While the unique attributes of certain technology companies may protect their competitive positions in a way that was not true in past cycles, valuations do matter.

Market Concentration Should Favor Active Managers

As explained above, we believe that the highly concentrated market returns will normalize, either from a downward resetting of the Magnificent 7, a broadening of gains among the other components of the S&P 500, or a combination of the two.

From our standpoint, this actually creates significant risk for passive owners of the S&P 500, as the components that drove the majority of returns in 2023 could see a reset. In contrast, owning a concentrated basket of high-quality companies, some of which have been left out of the rally of the past twelve months, should create a favorable setup for future returns assuming the economy continues to grow at a healthy clip and interest rates remain stable or even come down.

One relevant theme we have been highlighting recently as part of our Quality Growth investing framework is Quality Cyclical Growth companies. These are businesses that exhibit all of the characteristics of Quality Growth companies — secular tailwinds ensuring long-term revenue growth, high and improving margins and returns on capital, and a lack of reliance on debt to fund growth — but with more cyclical demand. These companies tend to see revenue and profit growth across each cycle, but many quality-focused investors avoid them out of fear of getting caught in a cyclical downdraft.

We actually view the cyclicality as an opportunity, as our longer investment time horizon allows us to buy when valuations are attractive and thus ideally generate significant returns in companies other managers may overlook. And because these companies operate in cyclical industries, we often get multiple “bites at the apple,” with each industry downturn presenting a new opportunity for investment. Admittedly, investing in Quality Cyclical Growth companies requires more nimble management to cope with the ups and downs of each cycle, but we have had success investing in these industries over the years, protecting on the downside and capturing upside. Industries that come to mind include semiconductors, transportation, life science tools, and digital advertising, just to name a few.

More broadly, we think more elevated market volatility favors active managers. The stock market has steadily seen greater volatility in recent years, while longer-term returns have remained relatively stable. There are many potential explanations for the higher volatility — from the rise of multi-strategy hedge funds (“pods”) and quantitative strategies obsessed with short-term returns, to a more concentrated market driven by mega caps, to the rise of online retail trading. Regardless of the cause, the result is massive short squeezes, punishing sell-offs, and higher share price volatility. We believe this volatility provides an opportunity for the patient investor to buy companies at artificially lower prices than would otherwise be the case and to profit more quickly as investors look to reinvest in the opportunity of the day.

Final Thoughts

We are heartened that our Quality Growth approach delivered solid returns for 2023, despite a whirlwind of issues and debates that could just as easily have distracted us from focusing on the long-term. We are confident that the market will continue to broaden, assuming a stable economic environment, and we will seek to take advantage of increased volatility while trying to protect against downturns.

Thank you as always for your continued support. We wish you health, happiness, and prosperity in the coming New Year.

—

Originally Posted January 23, 2024 – First Quarter Strategic Income Outlook: Immaculate Disinflation

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Osterweis Capital Management and is being posted with its permission. The views expressed in this material are solely those of the author and/or Osterweis Capital Management and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Hedge Funds

Hedge Funds are highly speculative, and investors may lose their entire investment.

{kind=link}