Although there is a lot of data on the calendar for the February 26 week, those with market moving potential are few. Much of the data will complete a picture already forming. Although the week ends with the first Friday of the month on March 1, it is not an Employment Friday. The monthly employment report is set for release at 8:30 ET on the following Friday, March 8.

There are more reports related to the housing market which should confirm that homebuyers are still out there. The chilling effect of a few weeks of increases in mortgage rates probably won’t be too visible yet. However, it may be that consumers are coming to accept that the rate for a 30-year fixed rate mortgage is going to be around 7 percent for some time yet. If so, those who are entering the housing market for whatever reasons this spring will have to accept the available mortgage rates – whether for a fixed-rate or adjustable-rate mortgage – and look for an opportunity to refinance later at a lower rate.

Data on sales of new single-family homes in January is at 10:00 ET on Monday. It should reflect the ongoing scarcity of housing inventory and some momentum from homebuyers who locked in a lower rate in December and act to exercise it before it expires. The push to get a contract in place before rate locks expire may also be visible in the pending home sales index at 10:00 ET on Thursday. The numbers for home prices in the FHFA house price index and Case-Shiller home price index at 10:00 ET on Tuesday are for December, and this is not the most current read. However, these should show that low housing inventory and modest demand are keeping home valuations higher and reducing home affordability for some buyers.

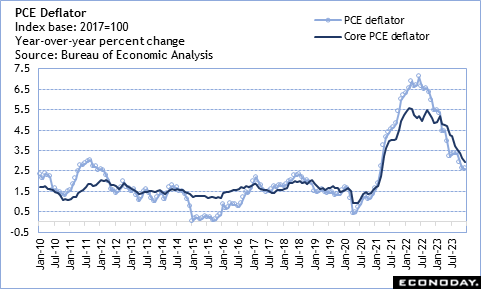

The second estimate of fourth quarter GDP is at 8:30 ET on Wednesday. Early estimates suggest little or no revision from 3.3 percent growth reported in the advance estimate. Fed policymakers are keeping a close eye on the continued string of stronger-than-expected growth in the US economy and whether the boost from solid consumer spending is likely to be maintained in 2024. The report on personal income and spending for January at 8:30 ET on Thursday is likely to suggest that households will have more income to spend. January incomes should see a solid increase from mandated rises in minimum wages that went into effect in December and January, end of year bonuses being paid out, and a 3.2 percent cost of living increase for social security recipients. Spending will see some increases related to inflation in services, but costs for durable and nondurables goods are generally trending lower. The PCE deflator probably will not show a lot of improvement from 2.6 percent year-over-year in the November and December reports, although the core PCE deflator could show continued easing in upward price pressures after 2.9 percent in December and 3.2 percent in November.

Conditions in the manufacturing sector in February seem to be improving. The manufacturing surveys from the New York and Philadelphia Feds point to a substantial lift from the prior month. However, these are two of the weaker correlations with the ISM manufacturing index. There are still the February reports from the Dallas Fed at 10:30 ET on Monday, Richmond Fed at 10:00 ET on Tuesday, and Kansas City Fed at 11:00 ET on Thursday.

—

Originally Posted February 23, 2024 – High points for US economic data scheduled for February 26 week

Disclosure: Econoday Inc.

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}