The post-earnings pop could prove intimidating to anyone waiting on the sidelines.

Congratulations are in order to anyone who was holding a stake in Shopify (SHOP 1.09%) before Aug. 7. The stock shot higher following Wednesday morning’s release of its second-quarter results, ending the day up a hefty 18%.

The big move raises an equally big question: Is it too late to buy Shopify stock?

In a word, nope.

Shopify shines again

Shopify helps companies of all sizes build and manage an e-commerce presence with services like web-based shopping carts, payment processing, etc. Estimates put the number of Shopify-powered online stores anywhere between 2 million and 4 million, which collectively serve millions of shoppers every single day.

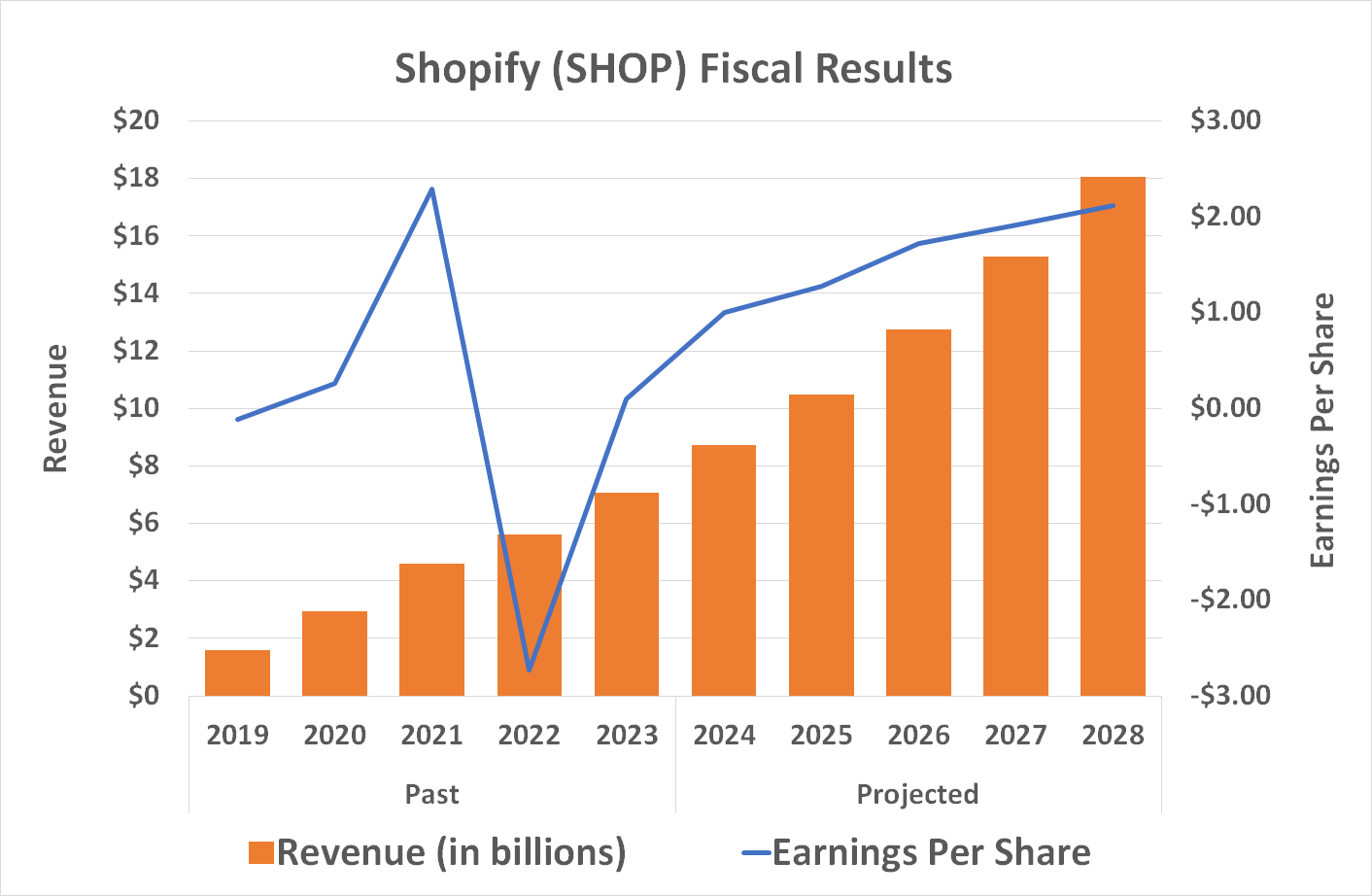

And they’re still shopping in droves. Last quarter, the company facilitated the sale of $67.2 billion worth of goods and services, collecting $2.0 billion of revenue for itself in the process. Those are 22% and 21% year-over-year improvements, respectively, and better than analysts were expecting.

Better still, Shopify swung back to a profit of $171 million after booking an accounting-driven loss in Q1, and management expects to continue growing both its top and bottom lines for the remainder of the year. Analysts agree, modeling 22% sales growth this year along with 32% earnings growth. Next year (and beyond) is expected to be just as impressive.

Data source: StockAnalysis.com. Chart by author.

And that’s the curious part of the Shopify story of late; despite healthy Q2 results and this week’s big gains, Shopify shares are still down about 25% from their February peak and down over 60% from their all-time high. What gives?

The latest leg of this weakness is the result of a lackluster Q1, or more specifically, the Q2 outlook shared in that report. The company said in May that it was only looking for Q2 sales growth in the high teens, down from its historical growth pace. CFO Jeff Hoffmeister’s discussion of “headwinds related to FX from the strong U.S. dollar and some softness in European consumer spending” further deflated investors, extending the weakness that first took hold a few weeks prior.

Now, the market’s realizing it may have made a mistake by giving up on Shopify so easily.

Catching a cyclical and secular tailwind

The core argument for owning a stake in this e-commerce technology company remains a numbers-based one. It’s demonstrated strong historical growth and is expected to continue growing for the foreseeable future. It’s also back to profitability following the earnings surge seen during the COVID-19 pandemic. Only this time, it’s built to stay in the black.

The other argument for owning a piece of Shopify, however, is a more philosophical one. That is, Shopify is already operating where e-commerce is going.

In the internet’s infancy, consumers and companies alike relied on platforms like eBay and Amazon to serve as a shopping intermediary. But time and technology are negating at least some of this reliance on such middlemen. Consumers are now finding products offered directly by brands themselves. Indeed, it’s arguable Amazon and eBay have become too big for many of their merchants’ own good, pitting them against one another (and in Amazon’s case, against the tech giant itself). Shopify offers the obvious alternative.

It’s only scratched the surface of its opportunity though. Shopify merchants’ stores only account for about one-tenth of the United States’ annual e-commerce sales and only about 6% of Western Europe’s (where it’s still relatively new) online-shopping industry. The rest is business to be won.

In the meantime, the e-commerce market itself continues to grow with plenty of room to continue doing so. The U.S. Census Bureau says less than 16% of the nation’s retail spending is currently done online. While some of it will always be done in-store, much of the remaining 84% is still up for grabs. Market research outfit Oberlo expects the U.S. e-commerce industry’s revenue to grow at a pace of 10.5% this year and then accelerate slightly every year through 2027.

Connect the dots, and you’ll see there’s still a lot of growth potential for Shopify to tap into here.

Plenty of upside

As promising as its business may be, owning Shopify stock is not for the faint of heart. Shares have experienced extreme volatility in the past several years.

For those willing to take the plunge, the key is to remain patient enough to let shares reflect how well this company is capitalizing on its opportunity.

If you’re still unsure, this might help. Of the 51 analysts covering Shopify stock, 30 recommend the stock as a buy, and the rest at least rate it a hold. None suggest selling. Consider making your move before the stock sees yet another bullish week.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Shopify. The Motley Fool recommends eBay. The Motley Fool has a disclosure policy.

{kind=link}