Wall Street’s enthusiasm for electric vehicles (EVs) isn’t what it was a couple of years ago. Shares of Chinese electric vehicle manufacturer Nio (NIO -7.69%) are down a staggering 90% from the high they reached in early 2021.

A growing fear surrounds China’s economy, with conditions marked by Chinese consumers reportedly struggling and spending less. But does all that justify Nio’s deep stock decline, or is this an opportunity to buy an up-and-coming company at bargain-basement prices?

Most recent sales data points to solid momentum

Nio primarily sells its EVs in its domestic Chinese market, but is expanding globally, including ramping up in Europe, and is weighing plans for the United States. The company’s EV line-up includes nine models of cars and SUVs. Nio has also pioneered a battery-swapping technology that can remove a drained battery and replace it with a fully charged one in approximately three minutes.

However, promising technology doesn’t necessarily translate to business success. Just ask Lucid Group (LCID -1.95%).

Investors can look at the sales data for honest feedback on how Nio is doing. In January, it delivered 10,055 units, an 18.2% year-over-year increase. The company’s Q4 deliveries were up 25% year over year. It doesn’t seem like Nio’s struggling to move its EVs.

That could change if Chinese consumers’ struggles worsen, but Nio is also expanding to international markets, which could offset some of that potential weakness. Additionally, the long-term trend of EV adoption remains strong in China. In November, new energy vehicles (battery EVs, hybrids, and fuel cell EVs) accounted for more than 40% of vehicle purchases — the first time they had exceeded that milestone.

Share price and fundamentals moving in opposite directions

It’s somewhat ironic that Nio’s share price has plummeted by 90% over the past two years while its revenue has nearly quadrupled. Nio isn’t profitable yet. But that’s normal when a business is spending billions on ramping up its manufacturing operations, and the overhead of such factories is expensive — they need to operate at capacity to be profitable.

NIO Revenue (TTM) data by YCharts.

The important thing is that Nio is continuing to grow its output and is selling what it does manufacture. Over time, its cash losses should slow, then pivot toward breakeven and eventual profitability.

Nio’s Q3 operating losses were $581 million, excluding stock-based compensation. The company has $6.2 billion in total cash and equivalents on the balance sheet, so investors don’t have to worry about it running out of cash.

Is Nio a buy, sell, or hold?

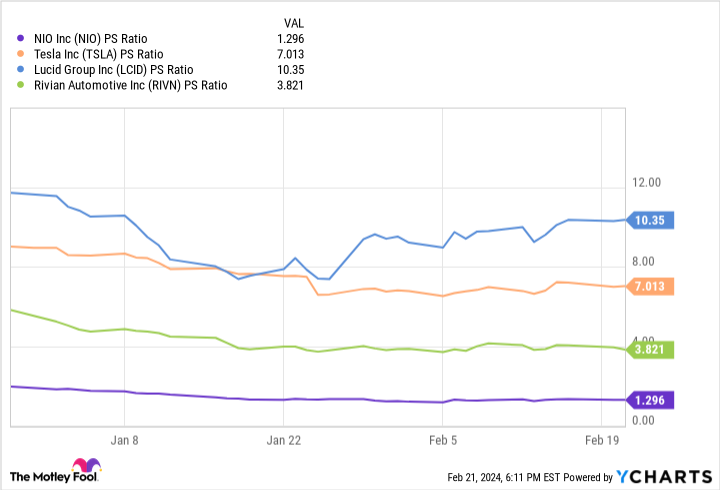

If you look at Nio’s price-to-sales ratio versus publicly traded competitors like Tesla, Rivian, and Lucid, Nio stands out as the cheapest by a wide margin. The question for investors is whether Nio deserves to be.

Based on Tesla’s profitability alone, I think it’s fair that the U.S. EV leader trades at a premium to Nio. But the others? Lucid delivered fewer cars in all of 2023 than Nio did last month. Lucid is facing a far longer road to grow its production, so for it to be trading at a P/S ratio more than five times higher than Nio’s doesn’t make sense. Rivian is also unprofitable and expects no sales growth in 2024.

NIO PS Ratio data by YCharts.

That’s not to say that Nio is a risk-free stock — the company will still need to execute at a high level for years if it’s going to succeed. But one could argue that Nio is getting punished excessively by investors, despite executing better than EV companies not named Tesla.

Nio looks like a far better buy than many of its peers for investors who are seeking long-term upside and who are comfortable holding Chinese companies in their portfolio.

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nio and Tesla. The Motley Fool has a disclosure policy.

{kind=link}