Dell Technologies‘ (DELL -1.33%) remarkable stock market rally came to a halt after the company released fiscal 2025 third-quarter results (for the three months ended Nov. 1) on Nov. 26, with shares of the technology giant that’s known for its personal computer (PC) and server solutions dropping more than 12% in a single day.

It wasn’t surprising to see investors pressing the panic button following Dell’s results. The stock has delivered outstanding gains so far this year thanks to its improving financial performance. Moreover, Dell’s growing artificial intelligence (AI) credentials have led to heightened expectations from the company. So, when Dell failed to deliver the numbers that Wall Street was looking for, the stock dropped big time.

However, this looks like an opportunity for savvy investors to buy a solid AI stock on the cheap. Let’s look at the reasons why.

The PC market is weighing Dell down, but investors shouldn’t miss the bigger picture

Dell reported fiscal third-quarter revenue of $24.4 billion, an increase of 10% from the year-ago quarter. The company’s non-GAAP (adjusted) earnings increased 14% year over year to $2.15 per share. Dell’s top line missed the midpoint of its quarterly revenue guidance of $24 billion to $25 billion in revenue by a whisker.

Analysts had set the bar even higher and were expecting Dell to deliver $24.7 billion in revenue. However, the company did beat the $2.06 earnings estimate comprehensively. Dell followed up its mixed quarterly numbers with weaker-than-expected guidance. The company is expecting fiscal Q4 revenue to land at $24.5 billion at the midpoint, which would be an increase of 10% from the year-ago quarter.

Analysts, however, were looking for $25.6 billion in revenue from Dell. The slower-than-expected recovery in the PC market was a key factor behind Dell’s lower-than-expected guidance. PC shipments in the third quarter of 2024 were down 2.4% from the prior-year period, according to market research firm IDC. Dell’s shipments were down 4% year over year.

This explains why the company’s revenue from the client solutions group (CSG), through which it sells desktops, notebooks, workstations, and other PC-related hardware, fell 1% year over year to $12.1 billion. Though Dell’s commercial PC revenue increased 3% from the year-ago period to $10.1 billion, slower-than-expected growth in consumer PCs weighed on this segment.

Dell points out that the PC refresh cycle has moved into 2025, and that’s the reason why its CSG business may take some time to step on the gas. However, Dell is confident of a turnaround in the consumer PC space, pointing out that tailwinds such as “an aging install base, AI-driven hardware enhancements like battery life, and Windows 10 end of life” are likely to inject some momentum into this market.

The growing adoption of AI PCs, in particular, is expected to play a key role in this market’s turnaround. Gartner estimates that AI PC shipments could increase an impressive 165% in 2025 to 114 million units, accounting for 43% of the overall market. So, there is a good chance that Dell will start witnessing growth in the CSG business next year.

At the same time, investors shouldn’t forget that the demand for Dell’s servers is increasing at an incredible pace thanks to AI. The strong demand for Dell’s AI servers led to a 34% year-over-year increase in the company’s revenue from the infrastructure solutions group (ISG) business to $11.4 billion. Sales of the company’s servers and networking solutions shot up 58% to $7.4 billion.

The company sold $2.9 billion worth of AI servers last quarter. More importantly, the demand for those servers was even stronger as it received a record $3.6 billion worth of orders for AI servers last quarter. Dell management also pointed out that its revenue pipeline of AI servers for the next five quarters increased by more than 50% on a sequential basis.

Looking ahead, AI servers should continue to move the needle in a significant way for Dell. That’s because the market for AI servers is expected to clock an annual growth rate of 30% through 2033, generating an annual revenue of $430 billion at the end of the forecast period.

The valuation makes buying Dell stock a no-brainer

Dell’s latest quarterly results may have evoked mixed emotions among investors, but the discussion above tells us that the company has terrific long-term prospects thanks to the growing adoption of AI in the server and PC markets. That’s the reason why buying Dell stock right now looks like a smart thing to do.

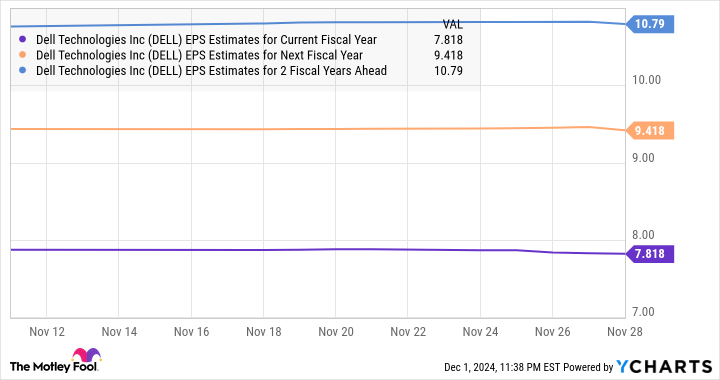

After all, Dell is trading at 22 times trailing earnings and 14 times forward earnings. Those multiples are lower than the tech-heavy Nasdaq-100 index’s 32 times trailing earnings and 29 times forward earnings. As the chart below tells us, Dell is expected to clock healthy double-digit earnings growth going forward.

DELL EPS Estimates for Current Fiscal Year data by YCharts

It won’t be surprising to see the stock sustaining this momentum for a longer period, considering the lucrative AI-related addressable markets that it is serving, which is why investors looking to buy an AI stock right now that’s trading at an attractive valuation should take a closer look at Dell before it regains its mojo.

{kind=link}