Warren Buffett fans eagerly anticipate Berkshire Hathaway‘s quarterly 13F filings, which tell investors what stocks the holding company bought and sold over a three-month period. The 2023 fourth-quarter filing was released last week, and it showed that Berkshire Hathaway sold out of four positions — Markel, Global Life, D.R. Horton, and StoneCo (STNE 2.00%).

Berkshire invested in StoneCo’s initial public offering (IPO) in 2018, and it’s down 48% since then. Did Buffett and his team give up on it? And what should other investors do now?

Why StoneCo looked like a good investment

StoneCo provides small business payment and management solutions in Brazil, and it has also expanded into a broader set of financial services like loans and bank accounts for its business clients. It has consistently reported increasing revenue and higher customer count, and it has a large market opportunity.

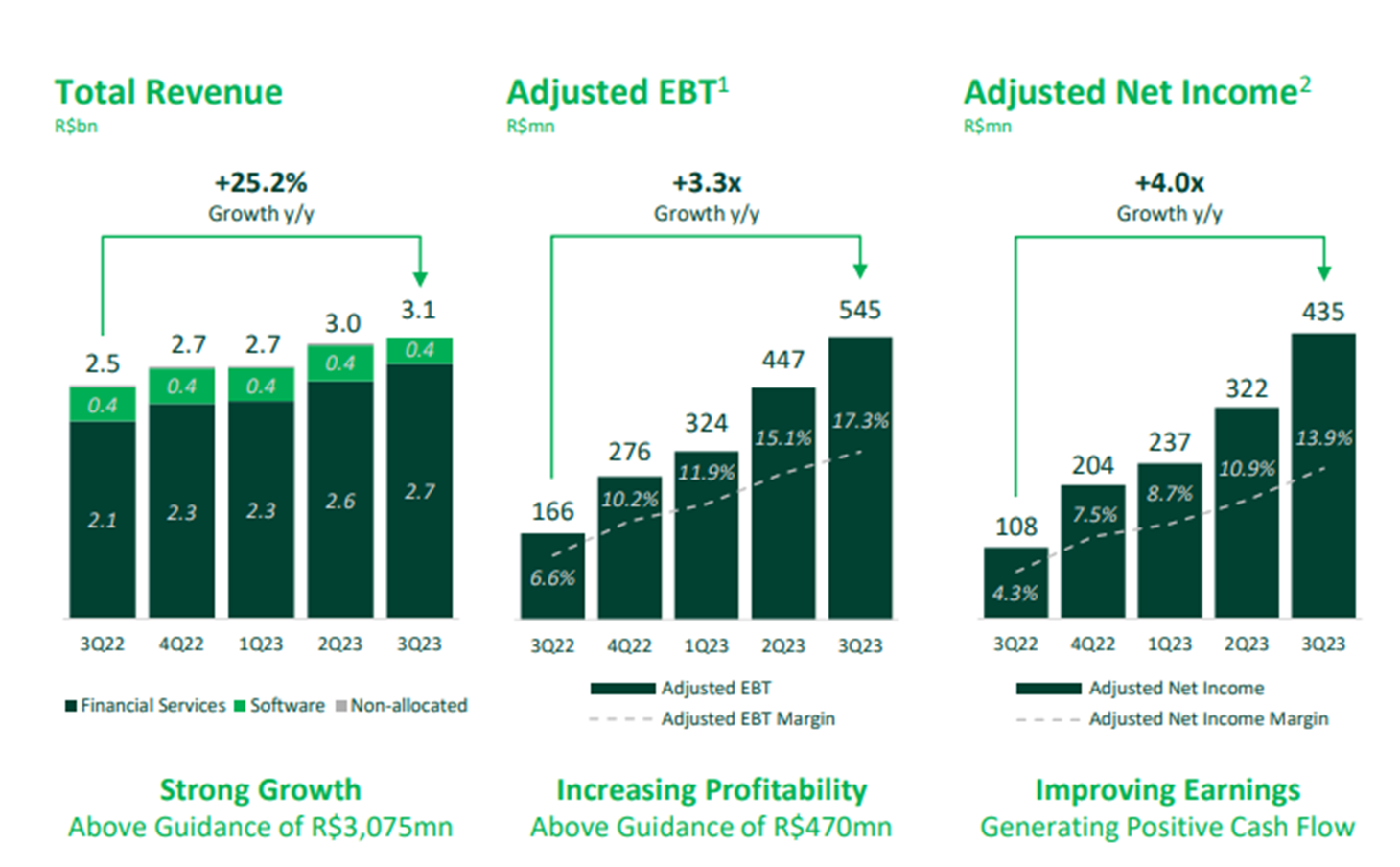

StoneCo doesn’t report fourth-quarter earnings for another few weeks, but its third quarter illustrated the trajectory. Revenue increased 25% year over year, and its payment client base increased 41%.

It’s also demonstrating improving profitability. Adjusted net income quadrupled from last year, and adjusted net income margin expanded from 4.3% to 13.9%.

Image source: StoneCo.

The future looks good — but far off

StoneCo has faced some major hurdles during the past few years due to regulatory changes in its home country of Brazil. It was slow to react to ensuing challenges, and the high default rates for its credit products cut into revenue and income. It has since dealt with these problems and strengthened its model, but not without scaring off some investors. On top of that, it’s been changing its executive team, which is a good step toward stabilization but presents its own challenges.

There is some inherent risk in investing in international companies, especially those in a country like Brazil, which has been dealing with persistent macroeconomic challenges.

StoneCo seems to be in a good place right now. It expects adjusted net income to increase at a compound annual growth rate of 35% through 2027. It has expanded its platform to target more medium-size and larger businesses, leading to improved profitability, and its digital model is resulting in lower customer acquisition costs and costs to serve.

It sees a market opportunity of 54 billion Brazilian reals (about $11 billion), of which it has less than 1% right now.

Why did Buffett sell?

Any speculation as to why Berkshire Hathaway sold is just that — speculation. StoneCo could have looked enticing originally because it addresses real pain points with solid execution. And it’s getting into banking services, which is a Buffett favorite. Berkshire invested in it at about the same time it invested in Nu Holdings, another Latin American financial stock, and both pose a huge opportunity in an underserved market.

I wondered only last week why Buffett was still holding on to StoneCo. Berkshire might have finally decided its travails are taking longer to fix than it thinks is reasonable. But Berkshire also sold out of some lower-risk stocks and purchased satellite radio broadcaster Sirius XM, which doesn’t fit the typical Buffett model.

Investors shouldn’t be scared off from StoneCo simply because it’s not the right stock for Berkshire Hathaway right now. It’s a holding company with specific intentions that will differ from an individual’s portfolio. Berkshire Hathaway sold out of Costco stock in 2020, and it’s doubled since then.

However, StoneCo does look risky for the average investor right now. There’s a lot of potential, but a lot to work through. Investors with a high appetite for risk might be interested in taking a small position right now, but most investors should wait for more stability before diving in.

Jennifer Saibil has positions in Nu. The Motley Fool has positions in and recommends Berkshire Hathaway, Costco Wholesale, Markel Group, and StoneCo. The Motley Fool recommends Nu. The Motley Fool has a disclosure policy.

{kind=link}